Another year has come and gone, but so have credit card changes.

In 2023, we saw new players enter the scene such as the OCBC INFINITY Cashback Card but along the same vein, we’ve also seen many of the best credit cards take the backseat due to some unsavoury changes – which is exactly what we’re going to address in this article.

Keep on reading to see which credit cards were affected in 2023. Spoiler alert: Many miles credit cards got nerfed.

Table of contents

- OCBC Rewards Card: Major changes from OCBC Titanium Rewards Card

- OCBC: Addition of conversion fees for selected cards

- AMEX HighFlyer Card & AMEX True Cashback Card: Grab-Pay top-ups

- HSBC Revolution Card: Change in bonus categories

- DBS Altitude Card: Removal of 3 mpd rate

- Instarem amaze Card: Addition of top-up fees

- No-Fee Citi PayAll: No rewards earned on welcome offers and limo rides

OCBC Rewards Card: Major changes from OCBC Titanium Rewards Card

The OCBC Titanium Rewards Card was under much scrutiny last year for bumping its annual bonus cap of 120,000 OCBC$ down to a monthly bonus cap of 10,000 OCBC$. However, it’s just been revealed that the OCBC Titanium Rewards Card will undergo other significant changes beyond that.

[New!] From 15 January 2024 onwards, the OCBC Titanium Rewards Card will be shedding its old coat and completely revamping it into the OCBC Rewards Card. Surprisingly, this new identity change comes with a whole slew of revised benefits too.

Annual bonus cap limited by a monthly bonus cap

Previously, the OCBC Titanium Rewards Card was coveted for its impressive 120,000 OCBC$ bonus cap per year. This allowed cardholders to be strategic with their card spend and “maximising” their bonus OCBC$ on big-ticket item expenditures.

Unfortunately in the latter half of 2023, this annual bonus cap became restricted to a bonus cap of 10,000 OCBC$ per calendar month instead. Even though you’re still entitled to earn up to 120,000 bonus OCBC$ annually, this limit is now further restricted to a maximum of 10,000 bonus OCBC$ per month.

New selected retailers per quarter

For starters, cardholders will now earn 15 OCBC$ per S$1 spend or 6 miles per S$1 spend (6 mpd) on selected retailer merchants per quarter. These merchants are expected to change every three months.

For this quarter (1 Jan to 31 Mar 2024), the exclusive merchants to earn 6 mpd on are Tangs and Shein. This means that you can earn up to 5,000 additional OCBC$ on top of your 10,000 bonus OCBC$ monthly cap.

Meanwhile, you can also earn 10 OCBC$ per S$1 spend (equivalent to 4 mpd or 2.78% cash rebate) on certain retail categories both online and in-stores. Here are the merchants eligible for bonus OCBC$:

|

Merchant category codes (MCCs)

|

|

|

MCC 5309

|

Duty Free Stores

|

|

MCC 5311

|

Department Stores

|

|

MCC 5611

|

Men’s and Boy’s Clothing and Accessories Stores

|

|

MCC 5621

|

Women’s Ready to Wear Stores

|

|

MCC 5631

|

Women’s Accessory and Specialty Stores

|

|

MCC 5641

|

Children’s and Infants’ Wear Stores

|

|

MCC 5651

|

Family Clothing Stores

|

|

MCC 5655

|

Sports and Riding Apparel Stores

|

|

MCC 5661

|

Shoe Stores

|

|

MCC 5691

|

Men’s and Women’s Clothing Stores

|

|

MCC 5699

|

Miscellaneous Apparel and Accessory Shops

|

|

MCC 5941

|

Sporting Goods Stores

|

|

MCC 5948

|

Luggage or Leather Goods Stores

|

But that’s not all. The following merchants below also qualify for bonus OCBC$, regardless of mode of payment unless specified:

|

Alibaba

|

Guardian

|

Shopee

|

|

AliExpress

|

Lazada

|

Taobao

|

|

Amazon

|

Mustafa Centre

|

TikTok Shop

|

|

Daigou

|

NTUC Unity

|

Watsons

|

|

Ezbuy

|

Qoo10

|

Note: Shopee Pay transactions (under MCC 5262) and grocery expenses (under MCC 5411) are not eligible for bonus OCBC$.

Selected OCBC cards: Implementation of conversion fees

|

|

Continuing the OCBC discussion, multiple OCBC credit cards are now subjected to conversion fees. Since 1 February 2023, OCBC ended its free miles transfer programme for the OCBC 90°N, OCBC VOYAGE, and OCBC Premier Visa Infinite Cards.

Each miles redemption is now charged a S$25 nett fee per conversion, irrespective of frequent flyer partner. To some, this was a minor concern whereas to others, it could’ve incited a major shift to their miles strategy.

Cards still offering free miles conversion include co-branded cards like KrisFlyer UOB Card, AMEX Singapore Airlines KrisFlyer Card, AMEX Singapore Airlines KrisFlyer Ascend Card, and certain travel cards like the HSBC TravelOne Card (until 31 May 2024).

AMEX HighFlyer Card and AMEX True Cashback Card: No more points for GrabPay top-ups

While we’re no stranger to GrabPay top-up exclusions, last year saw the AMEX HighFlyer Card and AMEX True Cashback Card finally hopping on the train too. Since 4 April 2023, GrabPay top-ups were excluded from earning rewards on both cards.

Currently, the only viable credit card left to earn on GrabPay top-ups is the UOB Absolute Cashback Card. Although it’s a reduced 0.3% cashback rate as opposed to the standard 1.7%, it’s still better than nothing.

See also: GrabPay Mastercard vs Other Credit & Debit Cards

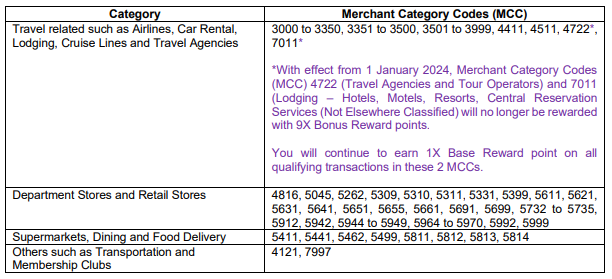

HSBC Revolution Card: No more 4 mpd for hotels and online travel agencies

Whether you’re new or a veteran in the miles chaser, the HSBC Revolution Card has been a staple miles credit card in many of our wallets – especially for travel-related bookings. But since 1 January 2024, it’s been nerfed to exclude selected hotels and online travel agencies (under MCCs 4722 and 7011) from earning bonus miles.

Source: HSBC

Now you can only earn the base 0.4 mpd rate on these transactions. Undoubtedly, this has left a little sour taste in our mouths.

But how did this situation arise in the first place? Well, the HSBC Revolution Card falls under the credit card minority where its MCCs follows a whitelist approach instead of a blacklist one. The former features a credit card’s merchant eligibility while the latter features a credit card’s merchant exclusions. Catching the drift?

Essentially, an MCC blacklist is preferable because as long as the merchant isn’t listed for exclusion, it’s good to earn bonus rewards. This effectively broadens the scope of eligible merchants for your credit card.

💡 Pro-tip: If the HSBC Revolution Card was your designated miles credit card for travel bookings, here are some other alternatives to consider instead: UOB Lady’s / Lady’s Solitaire Card, KrisFlyer UOB Card, Standard Chartered Rewards+ Card, Maybank Horizon Visa Signature Card, and of course, other travel credit cards.

DBS Altitude Card: Removal of bonus 3 mpd for airlines and hotels

DBS Altitude Visa Card

|

DBS Altitude AMEX Card

|

Another miles credit card to be hit hard by travel nerfs is the DBS Altitude Card. Previously, it was well-loved for its bonus 3 mpd earn rate on selected airlines and hotels. However, DBS has since revised this card’s mechanics and removed this bonus earn rate entirely.

Despite the increase in its earn rates from 1.2 mpd to 1.3 mpd (locally) and from 2 mpd to 2.2 mpd (overseas), this adjustment doesn't adequately compensate for the removal of the 3 mpd rate on travel bookings in our opinion.

The only relief in all this is that the DBS Altitude Card retained its bonus offerings of up to 10 mpd on Kaligo and Expedia bookings. Otherwise, these card changes have been lacklustre and somewhat disappointing.

Instarem amaze Card: E-wallet top-up fees

Since emerging on the market, the Instarem amaze Card has established its presence as a reliable multi-currency card. However, since 20 February 2023, all GrabPay, prepaid card, and other e-wallet top-ups started incurring a 2% fee (min. S$0.50) on all local transactions.

Since emerging on the market, the Instarem amaze Card has established its presence as a reliable multi-currency card. However, since 20 February 2023, all GrabPay, prepaid card, and other e-wallet top-ups started incurring a 2% fee (min. S$0.50) on all local transactions.

While this wasn’t the worst news, it was still kind of a downer.

No-Fee Citi PayAll: No rewards earned on welcome offers

For the uninitiated, Citi PayAll is a service that allows you to earn credit card rewards on your bill payments in situations where 1) credit cards aren’t normally accepted, and 2) when bills are excluded from earning rebates.

Within this service, you can opt for two options: No-Fee vs Fee-Paying. Although the No-Fee option appears the most tempting, its downsides are that you can’t earn any credit card rewards and it doesn’t count towards minimum spend requirements for credit card welcome offers and gifts.

For many, this defeats the appeal of using Citi PayAll to consolidate recurring bill payments.

If this shows us anything, it seems that the best things in life aren’t always free.

See also: Credit Card Promotions: Exclusive on SingSaver

Conclusion: Best credit card alternatives to consider

Overall, it seems that miles chasers were hit the hardest by credit card changes, whereas cashback lovers were treated to new launches like the OCBC INFINITY Cashback Card.

How many of these credit card changes were you affected by in 2023? And what are some credit card predictions you have for 2024? 🤔

Jump to:

Best Cashback Credit Cards (with min. spending and cap)

| Credit Card | Best for/Benefits | Details | Min. Annual Income |

|

Citi Cash Back Card

|

- 8% cashback on Petrol and Private Commute

- 6% cashback on Groceries and Dining

- 0.20% cashback on all other spending

|

- Min. S$800 monthly spend

- S$80 cashback cap (per statement month) - Annual fee: S$196.20 (First year free; 9% GST w.e.f. 1 Jan 2024) |

- Local/PR: S$30,000

- Foreigner: S$42,000

|

|

CIMB Visa Signature Card

|

- 10% cashback on Online Shopping, Groceries, Beauty & Wellness, Pet Shops & Vet services, and Cruises

- Unlimited 0.2% cashback for all other spending

|

- Min. S$800 monthly spend

- S$100 cashback cap (per statement month), and up to S$20 per category

- For spend beyond the cap, you will earn 0.2% cashback

- No annual fee

|

- Local/PR: S$30,000

|

|

Maybank Family & Friends Card

|

- 8% cashback on 5 selected categories:

1) Groceries 2) Dining & Food Delivery 3) Transport, Data Communication & Online TV Streaming 4) Retail & Pets 5) Online Fashion 6) Entertainment 7) Pharmacy 8) Sports & Sports 9) Apparels 10) Beauty & Wellness - 0.25% cashback on all other spending |

- Min. S$800 monthly spend

- S$125 cashback cap (per statement month), and up to S$25 per category

- Annual fee: S$181.67 (First 3 years free; 9% GST w.e.f. 1 Jan 2024)

|

- Local/PR: S$30,000

- Malaysian Citizen: S$45,000

- Foreigner: S$60,000

|

|

UOB EVOL Card

|

- 10% cashback on Online Spend

- 10% cashback on Mobile Contactless Spend

- 10% cashback on overseas in-store foreign currency spend

- 0.3% cashback on all other spending

|

- Min. S$800 monthly spend

- S$80 total cashback cap (per statement month)

- Annual fee: S$196.20 (Waived when you make a min. 3 transactions every month for 12 consecutive months)

|

- Local/PR: S$30,000

- Foreigner: S$40,000

|

|

OCBC 365 Card

|

- 5% cashback on Dining and Online Food Delivery

- 6% cashback on Petrol

- 3% cashback on Groceries, Land Transport, Utilities, Streaming, Drugstore and Electric Vehicle Charging

- 0.25% cashback on all other spending

|

- Min. S$800 & S$1,600 monthly spend

- S$80 & S$160 cashback cap depending on monthly spend tier (per statement month)

- Annual fee: S$196.20 (First 2 years free; 9% GST w.e.f. 1 Jan 2024)

|

- Local/PR: S$30,000

- Foreigner: S$45,000

|

Best Miles & Travel Credit Cards

Maximise your budget holiday spend even further with the best air miles credit cards and best credit cards for travelling in Singapore. Get rewarded whenever you spend locally or overseas, plus access awesome perks like airport lounges, discounted travel insurance rates, and even free gifts for first sign ups!

| Credit Card | Best for/Benefits | Details | Min. Annual Income |

|

Citi PremierMiles Card

.png?width=250&height=158&name=CITI_PREMIERMILES_MASTER%20(1).png)

|

- S$1 = 10 miles on Bookings at Kaligo

- S$1 = 7 miles on Hotel Bookings at Agoda - S$1 = 2 miles on Foreign Spend - S$1 = 1.2 miles on Local Spend

- 2 free airport lounge visits per year with Priority Pass

- Up to S$1 million complimentary Travel Insurance coverage when you charge travel tickets to card |

- Miles awarded as Citi Miles, which never expire

- S$27 per redemption - Annual fee: S$196.20 (First year free) |

- Local/PR: S$30,000

- Foreigner: S$42,000

|

|

DBS Altitude Card

|

- S$1 = 3 miles on Agoda Bookings

- S$1 = 2.2 miles on Foreign Spend - S$1 = 1.3 miles on Local Spend

- 2 free airport lounge visits per year with Priority Pass

|

- Miles awarded as DBS Points, which never expire

- 5,000 DBS Points = 10,000 KrisFlyer Miles

- S$27.25 (incl. GST) per redemption - Annual fee: S$196.20 (First year free)

|

- Local/PR: S$30,000

- Foreigner: S$45,000 |

|

OCBC 90°N Miles Card

|

- S$1 = 1.3 miles on Local Spend

- S$1 = 2.1 miles on Foreign Spend

- S$1 = 7 miles on Agoda Bookings in Foreign Currency

- S$1 = 6 miles on Agoda Bookings in Local Currency

|

- 90°N Miles never expire

- 1 90°N Mile = 1 KrisFlyer Mile

- 90°N Miles can be redeemed per blocks of 1,000 Miles

- Exchange 90°N Miles for cash rebates, vouchers, or offset travel costs too

- Annual fee: S$196.20 (Frist year free)

|

- Local/PR: S$30,000

- Foreigner = S$45,000

|

|

Maybank Horizon Visa Signature Card

|

- S$1 = 2.8 miles on Overseas Spend and Air Tickets (All Airlines)* - S$1 = 1.2 miles on Local Retail Spend^ on Shopping, Dining, Food Delivery, Supermarket, Transport, Hotels, Cruises, Travel Packages, Car Rentals - S$1 = 0.25 miles on Utilities, Education, Insurance, and Medical expenses - Complimentary access to Selected VIP Airport Lounges - Up to S$1 million Complimentary Travel Insurance Coverage |

- Min. S$800 spend per month required, otherwise 1.2 mpd only

- Miles awarded in the form of TREATS Points

- *Capped at 40,000 Bonus TREATS Points per calendar month for Air Tickets. Up to 3.2 mpd for a limited time only. T&Cs apply.

- ^No min. spend, no cap

- Annual fee: S$196.20 (First 3 years free)

|

- Local/PR: S$30,000

- Malaysian Citizen: S$45,000

- Foreigner: S$60,000

|

|

UOB PRVI Miles Card |

- S$1 = 6 miles on Selected Online and Flight Bookings at Agoda, Expedia, and UOB Travel

- S$1 = 2.4 miles on Overseas Spend - S$1 = 1.4 miles on Local Spend - Up to S$500,000 complimentary Travel Insurance Coverage |

- Miles awarded as UNI$

- S$25 per redemption

- Annual fee: S$261.60 (First year free)

|

- Local/PR: S$30,000

- Foreigner: S$40,000

|

|

HSBC TravelOne Card |

- S$1 = 2.4 miles on Foreign Spend

- S$1 = 1.2 miles on Local Spend

- 4 Complimentary Airport Lounge Visits per year (Primary cardholders only)

- Up to US$100,000 Complimentary Travel Insurance Coverage (including COVID-19)

|

25,000 Rewards Points = 10,000 Miles

5 free supplementary cards

No conversion fee for air miles or hotel points (Until 31 May 2024)

Annual fee: S$196.20 (First year free)

|

- Local/PR: S$30,000

- Foreigner/Self-Employed: S$40,000

|

|

Standard Chartered Journey Card |

- S$1 = 2 miles on Foreign Spend

- S$1 = 1.2 miles on Local Spend

- S$1 = 3 miles on Select Local Online Categories like Transportation, Grocery, and Food Delivery*

- 2 Complimentary Priority Pass Airport Lounge Visits per year

- Up to S$500,000 Complimentary Travel Insurance Coverage

|

- Rewards Points never earned from SC Journey Card never expire

- 25,000 Rewards Points = 10,000 KrisFlyer Miles

- *Capped at S$1,000 spend per statement month

- 45% off MSIG TravelEasy Travel Insurance (Single Trip) (Valid till 30 Jun 2024)

- Annual fee: S$196.20 (First year free)

|

- Local/PR: S$30,000

- Foreigner: S$60,000 |

|

KrisFlyer UOB Card |

- S$1 = 3 miles on Everyday Spend (e.g. Dining, Online Food Delivery, Online Shopping, Online Travel, Local Transport)*

- S$1 = 3 miles on Singapore Airlines, Scoot, KrisShop, and Kris+ purchases

- S$1 = 1.2 miles on All Other Spend

- Up to S$500,000 Complimentary Travel Insurance Coverage

- Fast track to KrisFlyer Elite Silver Status

- Other Membership Privileges on Scoot

|

- *Min. S$800 annual spend on Singapore Airlines, Scoot, and KrisShop required

- Earn KrisFlyer Miles directly to KrisFlyer Membership Account

- No cap on miles earned but only credited within 2 months of paying annual fee

- Annual fee: S$196.20 (First year free)

|

- Local/PR: S$30,000

- Foreigner: S$40,000

|

|

AMEX Singapore Airlines KrisFlyer Credit Card |

- S$1 = 1.1 miles on Local Spend - S$1 = 2 miles on Foreign Spend during June and December - S$1 = 2 miles on Singapore Airlines-Related Spend - S$1 = 3.1 miles on Grab Singapore Transactions, capped at S$200 per month -S$1 = 0.5 miles on Singapore Airlines Instalment Plans via PaySmall for eligible purchases - Up to S$350,000 Complimentary Travel Insurance coverage - Exclusive Hertz Gold Plus Rewards Loyalty Programme Perks |

- Earn KrisFlyer Miles directly to KrisFlyer Membership Account

- Annual fee: S$179.85 (First year free)

|

Subject to American Express' approval

|

|

AMEX Singapore Airlines KrisFlyer Credit Card

|

- S$1 = 1.2 miles on Local Spend - S$1 = 2 miles on Foreign Spend during June and December - S$1 = 2 miles on Singapore Airlines-Related Spend - S$1 = 3.2 miles on Grab Singapore Transactions, capped at S$200 per month - Up to S$1 million Complimentary Travel Insurance Coverage - Exclusive Hertz Gold Plus Rewards Loyalty Programme Perks |

- Earn KrisFlyer Miles directly to KrisFlyer Membership Account

- Annual fee: S$343.35 (First year free)

|

Subject to American Express' approval

|

|

HSBC Revolution Card |

- S$1 = 4 miles on Online and Contactless Spend (e.g.Shopping, Groceries, Dining, Food Delivery, Ride-hailing) - S$1 = 0.4 miles on All Other Spend - Up to S$300,000 Complimentary Travel Insurance Coverage |

- Capped at S$1,000 spend / 9,000 Bonus Rewards Points per calendar month

- No annual fee

|

- Local/PR: S$30,000

- Foreigner/Self-employed: S$40,000

|

|

Citi Rewards Card |

- S$1 = 4 miles on Selected Online Transactions (e.g. Shopping, Ride-hailing, Food Delivery, Groceries) and In-Store Shopping - S$1 = 4 miles on All Other Retail Spend - Up to S$1 million Complimentary Travel Insurance Coverage |

- Capped at S$1,000 spend / 9,000 Bonus Rewards Points per statement month

- Annual fee: S$196.20 (First year free)

|

- Local/PR: S$30,000

- Foreigner: S$42,000

|

Similar articles

Pros And Cons Of Keeping Your Savings In Your CPF Special Account

A Complete Guide To 24-Hour Clinics In Singapore

6 Best Ergonomic Pillows In Singapore 2022 (Neck Pain, Posture Fixes)

Approached by A ‘Claims Specialist’ After A Traffic Accident? Here’s What You Should Do

Have a More Comfortable Retirement Through Tax Optimisation: SRS

FIFA World Cup 2022 Subscription Prices & Promotions in Singapore (And Where You Can Watch For Free)

Travel Insurance Add-ons: Which Ones are Worth Your Money?

Student Credit Cards — Are They Worth Signing Up For in 2023?

Back to Blog

Back to Blog