5 Reasons Why Your First Credit Card Should Be An Unlimited Cashback Card

Updated: 26 Aug 2025

Written bySingSaver Team

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

We can all agree that acquiring your first credit card is an exciting step into adulthood. Not only is it a milestone of getting older, but it’s an indicator of greater financial freedom and disposable income generally. (Although, we must preface that this does not correlate with greater financial responsibility.)

But that’s beside the point; your first credit card poses as a significant asset in your wallet, unlocking new spending opportunities and access to a whole slew of bank discounts and offers. With so many different credit cards to choose from, it’s natural to feel a little intimidated trying to select the right card to suit your needs and preferences.

Miles might help to sponsor your next flight ticket while receiving reward gifts are nice too. But for card beginners, there are multiple reasons why an unlimited cashback card might be your winner instead!

Curious? Here are some of our reasons why we think an unlimited cashback credit card is a great card for young adults to have in their arsenal.

Find the right credit card for you in no time. 💳✨

Compare exclusive offers on SingSaver across cashback, miles, and rewards cards—plus enjoy stackable welcome gifts.

5 reasons to choose an unlimited cashback credit card as your first credit card

1. No minimum spend and no cashback cap

As a young adult just entering the workforce, you wouldn’t want to be overwhelmed by expenditure management. There should be minimal complications involved, with spending made convenient, simple, and fuss-free.

This explains why an unlimited cashback card fits the bill.

Normally, you’d have to hit the card’s minimum monthly spend to qualify for cashback. But unlimited cashback cards require neither a minimum spend nor a cashback cap. This means that cardholders can effortlessly earn cashback with every purchase without fretting over having to qualify for it by hitting a target amount each month.

The absence of a cashback cap also removes the hassle of mindfully switching between credit cards when limits are hit. For example, the UOB EVOL card has a total cashback cap of S$60 per month. Thus, once the S$80 has been fully attained, it acts as a signal to switch over to their other cashback, miles, or rewards cards to continue earning rebates in other manners.

In comparison, you’d never face such a predicament with an unlimited cashback card.

2. Greater cashback eligibility across categories…

It’s also widely known that unlimited cashback cards have greater eligibility across various spend categories. Typically, credit cards bear different mechanics emphasis since each card is created to meet different consumer demands and preferences. Some cards are marketed as grocery credit cards while others are more dining and online shopping centric.

Based on their expenditure purposes, these cards will have their own category eligibility and exclusions. How category eligibility works in credit cards is based on an institution’s or company’s Merchant Category Code (MCC). The criteria for what is or isn’t eligible are determined by the respective banks.

Common examples of MCC exclusions include (but are not limited to):

-

MCC 6529 to 6540: Quasi Cash/Financial Services (e.g. e-wallet top-ups, utilities, insurance premiums)

-

MCC 8211 to 8299: Education Institutions

-

MCC 9000 to 9999: Government Services

-

MCC 5993: Other Miscellaneous Purchases (e.g. cigar stores and stands)

Even then, this list of exclusions is not exhaustive. One bank’s classification of a merchant might differ from another bank’s. You’ll have to scrutinise each card’s T&Cs to identify the classifications accordingly.

Unfortunately, unlimited cashback cards aren’t immune to such spend exclusions either. But, there are some exceptions.

3. … Even e-wallet top-ups, insurance premiums, and bills

For instance, the AMEX True Cashback Card is the true champion of ‘limitless’ spending. (The UOB Absolute Cashback Card used to be too, but more on that later.) While other cards might not consider quasi-cash or quasi-financial services as eligible spending (for cashback, miles, or points), it has minimal spend exclusions.

💡 Pro-tip: Take advantage of AMEX’s 3% welcome cashback bonus on all eligible transactions (up to S$5,000) in the first six months of your AMEX True Cashback card approval.

The rebate rate will drop back down to 1.5% after either the S$5,000 spend limit is met or the six months are up, whichever comes first

[Update!] Unfortunately, from 6 May 2024 onwards, transactions like charity, education, government, healthcare, utilities, and other professional services will be reduced from the bonus 1.7% to a mere 0.3% cashback for the UOB Absolute Cashback Card.

Well, at least one redeeming quality remains: you can still foot recurring premiums under MCC 6300 (Insurance Sales, Underwriting, and Premiums) and earn 1.7% cashback – along with other regular spend categories like retail shopping, F&B, groceries, travel, transport, and others.

4. Great for big-ticket item purchases

Speaking of unlimited cashback, using such cards to fund your big-ticket purchases is also a great idea. Why? Because imagine buying your car with a regular cashback card; chances are you’d bust the rebate cap instantly on a >S$100,000 purchase.

Let’s take the Mitsubishi Space Star car as a case study.

-

Mitsubishi Space Star*

-

Average Open Market Value (OMV) = S$14,864

-

Excise Duty (20% of OMV) = S$2,972.80

-

GST (7% of OMV + Excise Duty) = S$1,249

-

Registration fee = S$220

-

Other charges = ~S$9,705

-

Cost of Cat A Certificate of Entitlement (COE) = S$87,889

Total car ownership cost = S$116,999

*Values as of August 2022

Assuming you purchase the car with DBS Live Fresh, common sense will tell you that its 6% cashback on eligible contactless transactions (capped at S$50) will immediately be hit. This is where an unlimited cashback card comes to the rescue!

Switching to the Standard Chartered Unlimited card rewards you with a limitless 1.5% cashback. You’ll effectively earn S$1,755 in rebates on the Mitsubishi Space Star purchase.

💡 Pro-tip: Double that figure (3% cashback) when you deposit funds into an Unlimited$aver account.

5. Same access to bank promos (as other credit cards)

All credit cards unlock cardholders with access to a catalogue of exclusive offers and promos offered by the issuing bank. Unless you hit the card’s minimum spend easily, why waste your budget by forcing yourself to increase expenses unnecessarily?

You’ll be able to spend comfortably with an unlimited cashback card and still capitalise on bank-specific discounts and rewards. Catch our drift?

Best unlimited cashback credit cards to apply for on SingSaver

If you’re still reading up until this point, you’re a real trooper! Allow us to recommend the best unlimited cashback cards for you to consider applying for.

|

Cashback credit card |

Perks |

|

1.7% cashback No spend exclusions |

|

|

1.5% cashback 3% welcome bonus cashback (capped at S$5,000 spend within first six months) |

|

|

1.6% cashback 10% welcome bonus cashback (min. S$800 spend within first two months) |

|

|

1.5% cashback 100% rebate when paying bills via SC EasyBill Up to S$277 extra cashback (min. S$200 spend within first 30 days) |

[UPDATE] UOB Absolute Cashback Card

As mentioned, the UOB Absolute Cashback Card offers 1.7% cashback with no minimum spend or cashback. It’s the current highest rebate offered on the market.

[Update!] Initially, it was heralded for its lack of spend exclusions, but now, what used to be its strongest selling point has been severely nerfed. From 6 May 2024 onwards, it no longer awards the bonus 1.7% on transactions like school fees, utilities, rent, e-wallet top-ups, and more. Instead, it'll only net you the base 0.3% cashback now.

SingSaver x UOB Absolute Cashback Card Exclusive Offer

Get S$60 Cash via PayNow when you apply for a UOB Absolute Cashback Card and make a min. spend of S$500 within the first 30 days of card approval. Promotion is valid for new-to-UOB credit cardmembers only. Valid till 31 July 2026. T&Cs apply.

AMEX True Cashback Card

The AMEX True Cashback Card offers 1.5% cashback on all eligible spending, with no minimum spend or cashback cap. Compared to UOB Absolute Cashback, it’s not totally immune to spend exclusions. There are certain non-eligible categories like balance transfers, annual card fees, cash advance loans and others.

While 1.5% is the base rebate rate, this card sets itself apart thanks to the generous 3% welcome bonus cashback on the first S$5,000 eligible spend within six months of card approval.

Thanks to this bonus, cardholders can earn a maximum of S$150 rebate in those months.

Citi Cash Back+ Card

Another crowd favourite, the Citi Cash Back+ is a mid-tier card because of its 1.6% cashback with no minimum spend or cashback cap. Unfortunately, this card has considerably more spend exclusions than the aforementioned ones.

You can redeem your cash instantly on the go via SMS in rebate values of S$10, S$20, and S$50.

In any case, it’s still a decent cashback card to funnel all your retail spending towards. But if you need some convincing, give our Citi Cash Back+ card review a read.

SingSaver Citi Credit Card + Banking Bundle Offer

Score S$500 Cash via PayNow in place of exisiting rewards when you apply for a Citi Credit Card, make a minimum spend of S$500 and hold a valid Citi banking account (existing or newly opened) by the end of the month following card approval. Valid till 31 July 2026. T&Cs apply.

SingSaver Exclusive Offer

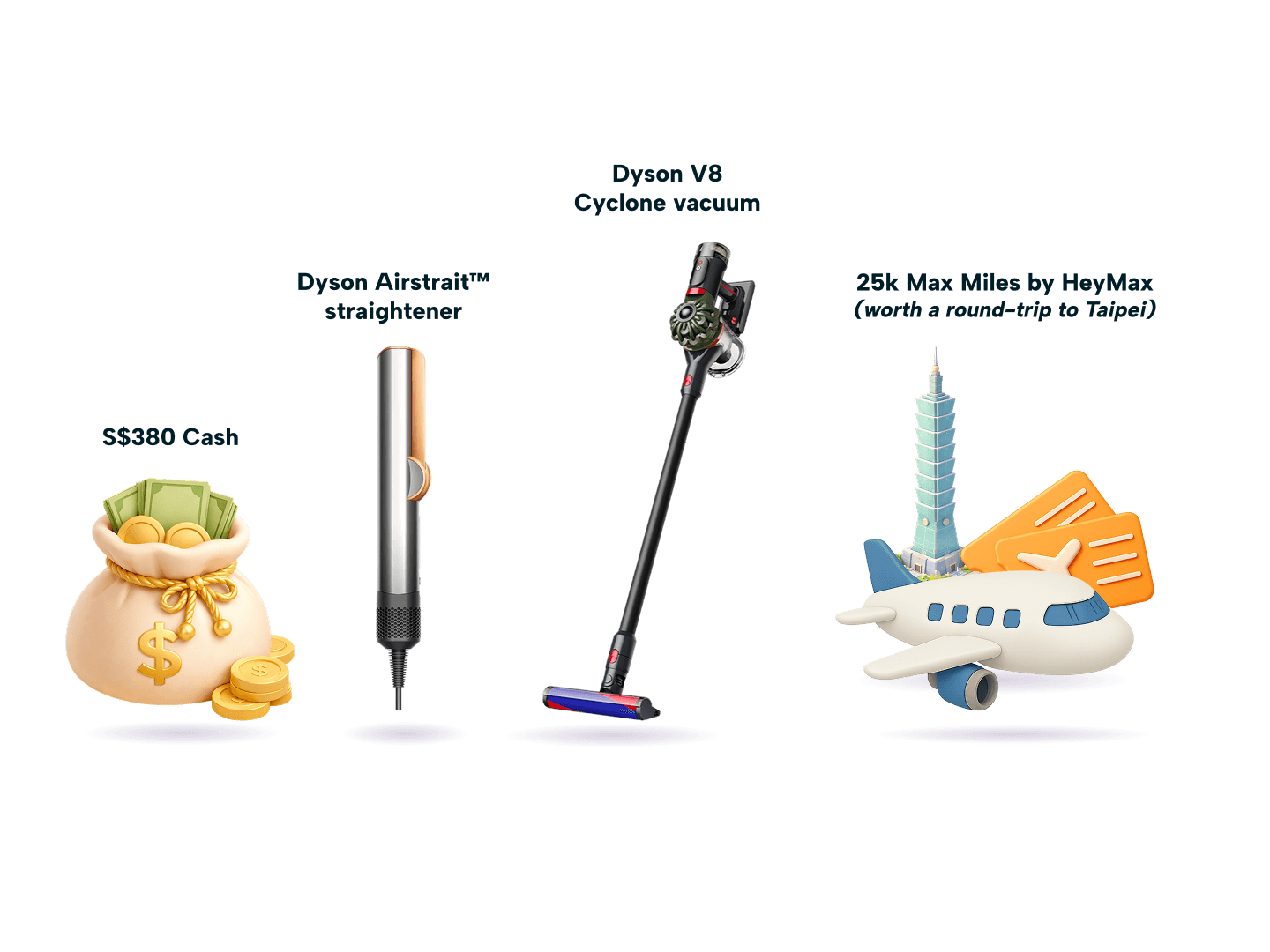

Apply for a Citi Cashback+ Credit Card via SingSaver and score upsized S$420 Cash, 25,000 Max Miles by HeyMax (worth S$600 in travel value), Dyson Airstrait or V8 Cyclone cordless vacuum, or Sony WF-1000XM6 (Earbuds) + S$80 eCap bundle upon activating and spending a minimum of S$500 within 30 days of card approval. Valid till 16 July 2026. T&Cs apply.

Or, Get the Reward Upgrade You Deserve!

You can also top up from just S$100 to upgrade to the latest Dyson and Apple products, including the latest MacBook Neo 256GB Magic Keyboard. Valid till 2 August 2026. T&Cs apply.

Standard Chartered Simply Cash Card

Last but not least, the Standard Chartered Simply Cash Card is another respectable card featuring 1.5% cashback with no minimum spend or cashback cap.

One of its perks includes full cashback when you pay your bills through SC EasyBill function. Furthermore, get up to S$277 rebate when you activate your physical card and spend S$200 on eligible merchants within 30 days of card approval.

If you need further information, maybe our Standard Chartered Unlimited Credit Card review can help.

SingSaver x SCB Simply Cash Card Exclusive Offer

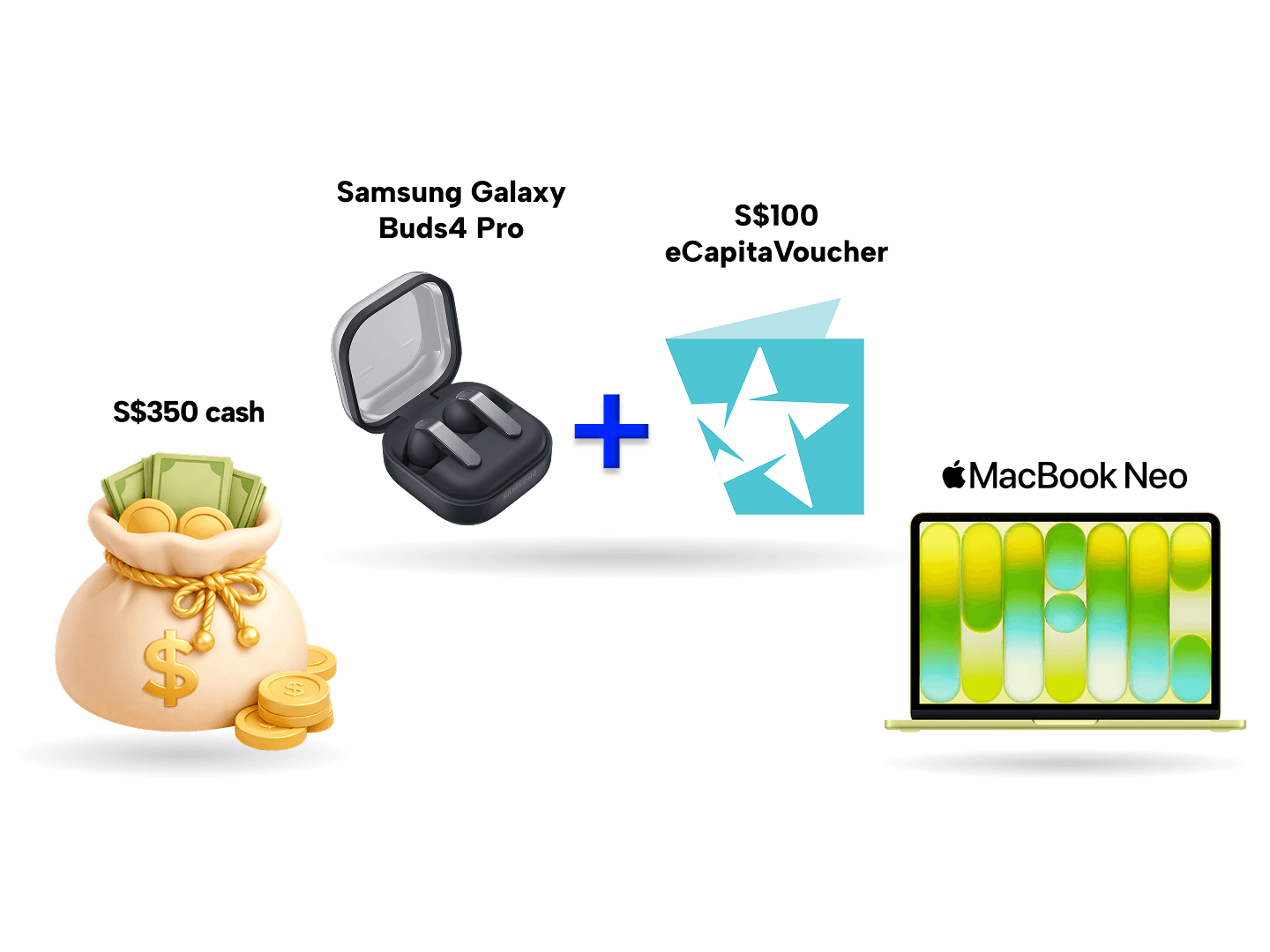

Get a Samsung Galaxy Buds4 Pro + 100 eCap bundle (worth S$449) or up to S$370 when you apply for a Standard Chartered Simply Cash Credit Card via SingSaver, spend a minimum of S$800 within 30 days of card approval, and apply for one of these products: EasyPay, Bonus$aver Account, CashOne, or CCFT. Valid till 2 August 2026. T&Cs apply.

Or, Get the Reward Upgrade You Deserve!

You can also top up from just S$100 to upgrade to the latest Dyson and Apple products, including the latest MacBook Neo 256GB Magic Keyboard. Valid till 2 August 2026. T&Cs apply.

Card | Hot Reward Pick | SingSaver Reward | Cashback Local | Cashback Overseas | Monthly Spend Required | Annual Fee | ||

|---|---|---|---|---|---|---|---|---|

| Standard Chartered Simply Cash Credit Card | S$699 | 1.5 % | 1.5 % | None | S$196.20 | ||

| UOB Absolute Cashback Card | S$160 | Up to1.7 % | Up to1.7 % | None | S$196.20 | ||

| Citi Cash Back+ Card | S$1,299 | Up to3.25 % | 1.6 % | None | S$196.20 | ||

| American Express True Cashback Card | - | - | 1.5 % | 1.5 % | None | S$174.40 |

Summary: Simplicity is key

Now, this must’ve been a lot of information to digest. Learning about new concepts like monthly bills, minimum payments, and annual fees as personal finance beginners and novices can be intimidating and tough.

But hopefully, we’ve managed to deconstruct how general cashback mechanics work and explain why an unlimited cashback credit card is a good first choice.

To reiterate, your first credit card should be straightforward to use. It shouldn’t involve you jumping through multiple hoops to satisfy rebate conditions. A limitless cashback card drowns out all the noise of minimum spend, cashback caps, differing categorical rebate rates and spend exclusions.

It simplifies everything into an easy-to-use and fuss-free card that’s effective for both everyday and major expenses. But as always, remember to read the fine print of your bank’s T&Cs if you’re unsure about eligible purchases!

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.