6 Best Supplementary Credit Cards To Gift Your Partner Or Kids

Updated: 11 Apr 2025

Every spending situation is unique. SingSaver assembles the 'Best For' list, so you can decide what’s best for you.

Written bySingSaver Team

Team

New to supplementary credit cards? Learn how they can offer added convenience and benefits for your family and loved ones while helping you manage household expenses.

| Best supplementary credit cards on SingSaver: SCB Simply Cash Card | UOB PRVI Miles AMEX Card | UOB One Card | Citi PremierMiles Card | OCBC 365 Card | HSBC Advance Card |

Supplementary credit cards can be a great financial tool in any household as they allow the primary cardholder to share credit card benefits and perks with their loved ones, most commonly their family members, spouse or children.

This type of credit card is linked to a primary credit card and typically shares the same reward structure. For example, if you earn 5% cashback on dining with your primary card, the supplementary card member will also enjoy this perk.

They also allow the supplementary cardmember to enjoy some or all of the same perks and privileges as the primary cardmember, although the degree to which this applies varies somewhat between providers.

In this article, we'll examine the pros and cons of supplementary cards and six popular cards you could consider extending to your loved ones.

What is a supplementary card?

If you've gotten a credit card already, you're likely qualified to sign up for a supplementary card. These cards can be assigned to a supplementary cardholder, like your spouse or child. As previously mentioned, these supplementary cards share the same reward perks and structure as your primary card, although there may be instances where the benefits do not apply to the supplementary cardholder. One example is the number of free visits to airport lounges.

It is also important to note that supplementary cards do not have their own bonus caps. Instead, the bonus cap is shared with the primary credit card. For example, if a credit card has a S$1,000 bonus spending cap, it will be shared between both the primary and supplementary cards.

Applying for one is pretty straightforward. You can either apply online or send in a form by mail. You might even snag rewards like bonus miles or cashback when you get a supplementary card. And don't stress about the costs—as many of these supplementary cards are free or have a low annual fee.

Using a supplementary credit card is no different than using a debit or credit card. However, do note that all transactions made with a supplementary card will appear on the main cardholder's billing statement, making the primary cardholder responsible for covering all the charges associated with the supplementary card. Supplementary cards also have no impact on the credit score of the supplementary card member.

If a payment is missed, only the credit score of the primary card member will be affected. Similarly, paying the supplementary cardmember's bill on time will enhance the credit score of the primary cardmember.

Lastly, all rewards earned through the supplementary card will be channelled to the primary card member's account. This means any cashback, air miles or rewards points will be credited back to the primary card, and the supplementary cardholder will not be able to use them.

Advantages and disadvantages of a supplementary card

|

Advantages |

Disadvantages |

|

Earn rewards faster |

Risk of overspending |

|

Switching one primary card to a supplementary card can result in a reduction of their total annual fees. |

Rewards earned are funnelled to the primary card member. |

|

Supplementary cardholders may use the card as a source of emergency money. |

Rewards caps are not increased. |

|

As supplementary cards have adjustable credit limits, you can use them to teach children how to set and manage budgets. |

The primary cardholder is responsible for paying charges on any supplementary cards. |

6 popular supplementary credit cards to get

|

Credit card |

Supplementary card annual fee |

Noteworthy rewards or perks |

|

Standard Chartered Simply Cash Supplementary Card

|

First 5 cards free |

1.5% cashback on all spends, no cap |

|

UOB PRVI Miles American Express Card |

First card free S$129.60 per card thereafter

|

1.4 miles per dollar on local spend 2.4 miles per dollar on overseas spend Up to 6 miles per dollar on hotel bookings

|

|

UOB One Supplementary Card |

First card free, S$97.20 per card thereafter |

New-to-UOB cardmembers |

|

Citi PremierMiles Supplementary Card |

Free for life |

1.2 miles per dollar on local spends 2 miles per dollar on overseas spends Up to 10 miles per dollar on hotel bookings

|

|

OCBC 365 Supplementary Card |

Free for up to 2 years S$97.20 thereafter |

6% cashback on petrol 5% cashback on dining and online food delivery 3% cashback on groceries, transport, recurring telco and electricity bills, pharmacy purchases, streaming services, electric vehicle charging Cashback capped at S$80/S$160 with S$800/S$1,600 minimum spend |

|

HSBC Advance Card |

First 5 cards free |

2.5% cashback when you spend more than S$2,000 per month, capped at S$70 per month Otherwise, 1.5% cashback with no min. spend Extra 1% HSBC Everyday+ Cashback when you deposit min. S$2,000 funds into HSBC EGA per month and make 5 eligible transactions per month |

#1: Standard Chartered Simply Cash Supplementary Credit Card

The SCB Simply Cash Credit Card gives you 1.5% cashback on all your spending, so the more transactions you charge to it, the more savings you’ll get.

This is also why this makes a great supplementary card for your family members. Put a copy into the hands of your spouse and children – which is easy to do as annual fees are waived for up to five supplementary cards – and watch the savings rack up!

SingSaver x SCB Simply Cash Card Exclusive Offer

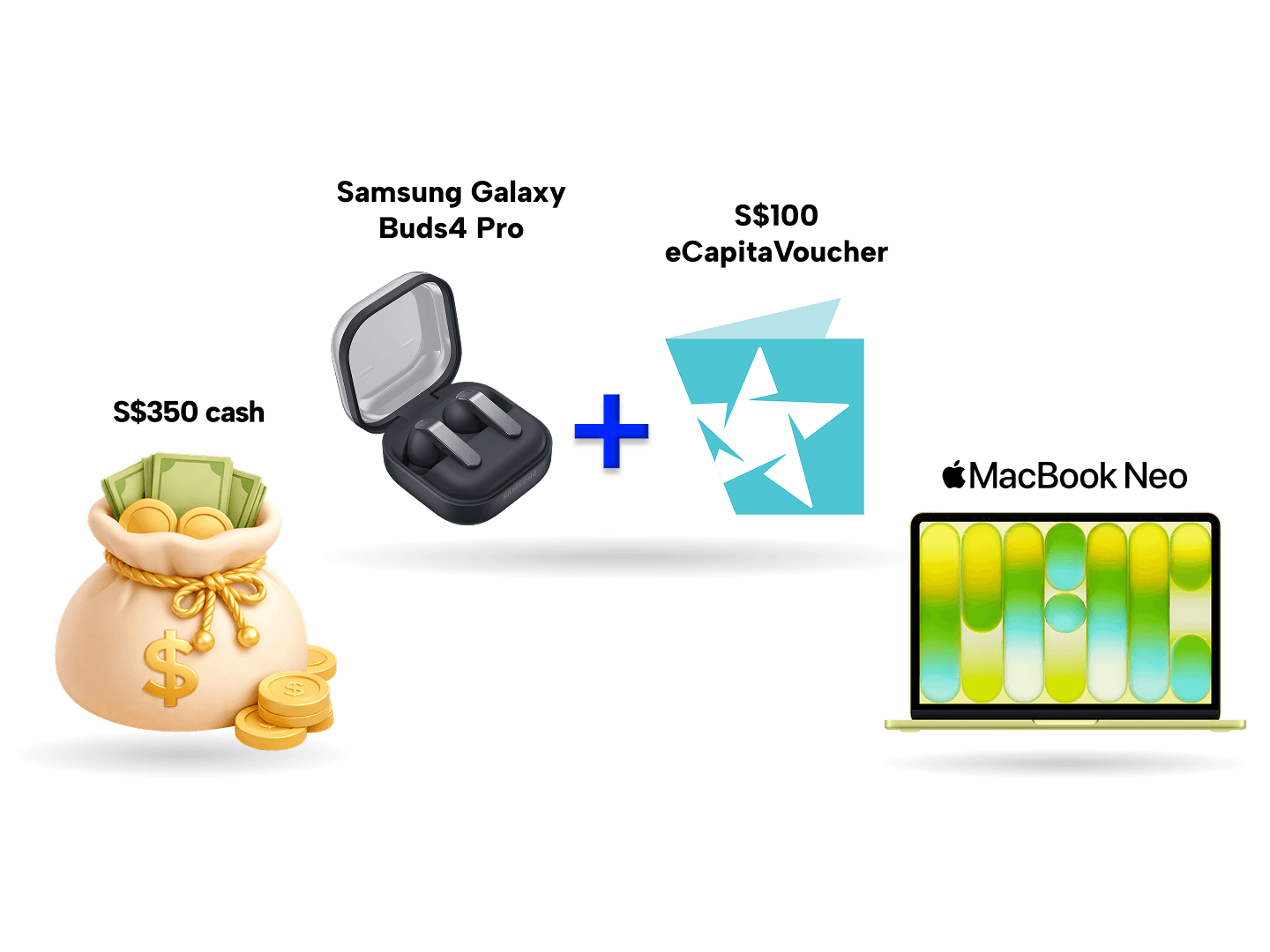

Get a Samsung Galaxy Buds4 Pro + 100 eCap bundle (worth S$449) or up to S$370 when you apply for a Standard Chartered Simply Cash Credit Card via SingSaver, spend a minimum of S$800 within 30 days of card approval, and apply for one of these products: EasyPay, Bonus$aver Account, CashOne, or CCFT. Valid till 2 August 2026. T&Cs apply.

Or, Get the Reward Upgrade You Deserve!

You can also top up from just S$100 to upgrade to the latest Dyson and Apple products, including the latest MacBook Neo 256GB Magic Keyboard. Valid till 2 August 2026. T&Cs apply.

#2: UOB PRVI Miles American Express Credit Card

The UOB PRVI Miles credit cards are known for their industry-leading local spend earn rate of 1.4 miles per dollar and 2.4 miles per dollar on overseas spending, including online shopping on overseas websites. It also rewards a remarkable 6 miles per dollar on major airlines and hotels via Agoda, Expedia, and UOB Travel.

But amidst all these rewards, perhaps it’s the American Express variant that makes having supplementary cards rewarding.

See also: Best American Express Credit Cards in Singapore (2023)

You’ll be awarded 50,000 air miles if you pay your primary card's first year's annual fee. Otherwise, you'll still earn 30,000 air miles if you choose to waive it. For context, a return-way Economy Saver Award Ticket from Singapore to

Seoul is worth 54,000 KrisFlyer miles already. So by paying the annual fee, you're only 4,000 miles away from redeeming a solo trip to Korea next year. 🤑✈️

Meanwhile, for the supplementary cards, only the annual fees for the first supplementary card can be waived.

UOB PRVI Miles Amex Card Welcome Gift: Get up to 58,000 miles when you successfully apply for a UOB PRVI Miles Amex Card, pay the annual fee, and spend a minimum of S$2,000 per month for two consecutive months. SMS registration is required. Valid for new-to-UOB credit cardmembers only. Valid till 31 January 2025. T&Cs apply.

Or, receive up to 38,000 miles when you successfully apply for the card, spend a minimum of S$2,000 per month for two consecutive months, and waive the annual fee. Capped at first 50 eligible cardmembers monthly. Valid for new-to-UOB credit cardmembers only. Valid till 31 January 2025. T&Cs apply.

#3: UOB One Credit Card

The rebate structure of the UOB One Card may take some working out, but the gist is this: spend at least S$500, S$1,000 or S$2,000 per month for three consecutive months (5 eligible transactions per month), and it will let you earn the maximum 15% quarterly cashback.

This insane cashback rate is only valid for new-to-UOB cardmembers. Existing members can only earn a maximum rate of 10% cashback.

But overall, keeping your spending up as long as possible will be the most rewarding way to use this supplementary card.

If you're struggling to hit the minimum monthly spend quotas, this is where your family members come in: rope them in to add their spending to the pool to fulfil the S$500, S$1,000, or S$2,000 monthly spend and get the most cashback possible each quarter.

UOB One Credit Card Welcome Gift: Get up to 20% enhanced cashback on daily favourites (i.e., DFI Retail Group, Grab, McDonald’s, Shopee Singapore and SimplyGo) when you successfully apply for the UOB One Credit Card. Enhanced cashback will be capped at S$100 per month for the first quarter. Valid till 31 January 2025. T&Cs apply.

#4: Citi PremierMiles Credit Card

The Citi PremierMiles Card lets you earn air miles at 1.2 miles per dollar spent locally, and 2 miles per dollar overseas.

And the best part is? All supplementary cards are free for life for Citi PremierMiles, so why not get your spouse and (fiscally responsible) kids a piece each and earn air miles on their spending, too?

| 💡Pro-tip: The Citi Prestige Card is another option that permits free supplementary cards for life. |

And if you’re worried about a glut of miles, don’t: Citi Miles have no expiry date.

SingSaver Exclusive Offer

Apply for a Citi PremierMiles Card via SingSaver and score upsized S$420 Cash, 25,000 Max Miles by HeyMax (worth S$600 in travel value), Dyson Airstrait or V8 Cyclone cordless vacuum, or Sony WF-1000XM6 (Earbuds) + S$80 eCap bundle upon activating and spending a minimum of S$500 within 30 days of card approval. Valid till 12 July 2026. T&Cs apply.

Or, Get the Reward Upgrade You Deserve!

You can also top up from just S$100 to upgrade to the latest Dyson and Apple products, including the latest MacBook Neo 256GB Magic Keyboard. Valid till 2 August 2026. T&Cs apply.

#5: OCBC 365 Credit Card

The OCBC 365 Credit Card offers up to S$160 cashback each month (or S$1,920 a year, not bad!), but you’ll have to spend at least S$1,600 monthly to get the cashback.

S$1,600 is a high monthly minimum to hit – but fret not. If you hit the first tier of a monthly S$800 monthly spend, you stand to get S$80 cashback each month, which is pretty decent as well.

Despite the slightly higher-than-average minimum monthly spend, some like it for the fact that there is no categorical limit on cashback earning, unlike other cards.

Recruit your family members to help you hit the monthly cap by pooling their transactions, especially if they frequently pay for online food delivery and dining (5% cashback), all petrol (6% cashback), groceries (3% cashback), Grab rides (3% cashback) and utility bills (3% cashback).

It’s somewhat of a pity that the OCBC 365 supplementary card annual fees are waived only for the first two years. If you really want to save on the annual fee, maybe put your children on rotation with this card.

SingSaver x OCBC 365 Credit Card Exclusive Offer

Apply for an OCBC 365 Credit Card via SingSaver and choose from S$400 Cash, 25,000 MaxMiles by HeyMax (worth S$600 in travel value), Dyson Airstrait, Dyson V8 Cyclone cordless vacuum, or Samsung Galaxy Buds4 Pro + S$180 eCapitaVoucher Bundle. Valid till 2 August 2026. T&Cs apply.

Or, Get the Reward Upgrade You Deserve!

You can also top up from just S$80 to upgrade to the latest Dyson and Apple products, including the latest MacBook Neo 256GB Magic Keyboard. Valid till 2 August 2026. T&Cs apply.

#6: HSBC Advance Credit Card

The HSBC Advance Credit Card gives 1.5% cashback on all your spending, rising to 2.5% when you spend more than S$2,000 a month.

If you can’t quite hit this limit on your own, get your spouse and/or children supplementary cards to pool their purchases. And since you can apply for up to five supplementary cards free, there’s little reason not to.

While your base cashback is capped at S$70 per calendar month, you can earn an additional 1% HSBC Everyday+ Cashback for a maximum of 3.5% cashback when you fulfil the following criteria:

-

Deposit fresh funds to your HSBC Everyday Global Account every calendar month via salary crediting and/or inward transfers from a non-HSBC bank account (minimum S$2,000 for HSBC Personal Banking customers and S$5,000 for HSBC Premier and Jade customers)

-

Perform a minimum of five eligible transactions every calendar month.

The maximum bonus cashback per calendar month is capped at S$300 for HSBC Personal Banking customers, and S$500 for HSBC Premier and Jade customers.

SingSaver x HSBC Advance Credit Card Exclusive Offer

Score S$420 Upsized Cash, Dyson Airstait or V8 Cyclone cordless vacuum, 25,000 Max Miles by HeyMax (worth S$600 in travel value), or a Ninja Speedi 10-in-1 Rapid Cooker & Air Fryer - ON401 when you apply for an HSBC Advance Credit Card via SingSaver and fulfil promo requirements. Valid until 2 August 2026. T&Cs apply.

Or, Get the Reward Upgrade You Deserve!

You can also top up from just S$100 to upgrade to the latest Dyson, Sony, and Apple products, including the latest MacBook Neo 256GB Magic Keyboard. Valid till 2 August 2026. T&Cs apply.

Frequently asked questions about supplementary credit cards

A supplementary credit card is an extension of your own credit card—linked to your primary card account and allows another person, usually a family member, to spend using your credit limit.

This means they can enjoy the same benefits as you, like rewards and cashback, while you retain control over the spending.

Most banks will allow you to issue supplementary cards to your immediate family members, such as your spouse or children.

Supplementary credit cards allow your family members to enjoy the perks of your primary card, like earning rewards and cashback. Plus, by pooling your spending, you can reach minimum spend requirements faster and unlock bonus rewards or cashback! It’s a win-win for everyone!

No—you'll receive one combined statement for all the spending on your primary and supplementary cards. This makes it easy to track everyone's expenses in one place.

Unfortunately, no. Since the account is under your name, your supplementary cardholder's spending activity won't affect their credit history.

Some banks offer supplementary cards with no annual fees, while others might charge a fee after the first year or for additional cards. Be sure to check the card details before you apply.

Yes! Any spending on your supplementary cards is combined with your primary card spending. This means you'll earn rewards faster and reach those minimum spending thresholds for bonuses more easily.

Applying for a supplementary credit card is usually a breeze. You can typically apply online through your bank's website or mobile app.

Alternatively, you can contact your bank's customer service hotline, and they'll guide you through the process. Just be prepared to provide some personal details of the person you want to add as a supplementary cardholder.

While supplementary cards offer great convenience and benefits, it's important to remember that you, as the primary cardholder, are ultimately responsible for all the charges. So, keep an eye on the spending to make sure you don't overspend or accumulate unnecessary debt.

Your primary credit card is the "basic" card that everything revolves around. A supplementary card is like an add-on to your basic card, allowing your family members to enjoy the same benefits and convenience while you manage the expenses and earn rewards on their spending.

The primary cardholder is the main person responsible for the credit card account. They're the ones who applied for the card and are liable for all the charges. A supplementary cardholder, on the other hand, is authorised to use the card but isn't responsible for the bills or account management. It's a great way to share card benefits with family members while maintaining control over the account.

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.