Singapore's official retirement age is gradually being raised from the current age of 62 to 65 by 2030. Here are two alternative scenarios to consider when planning for retirement.

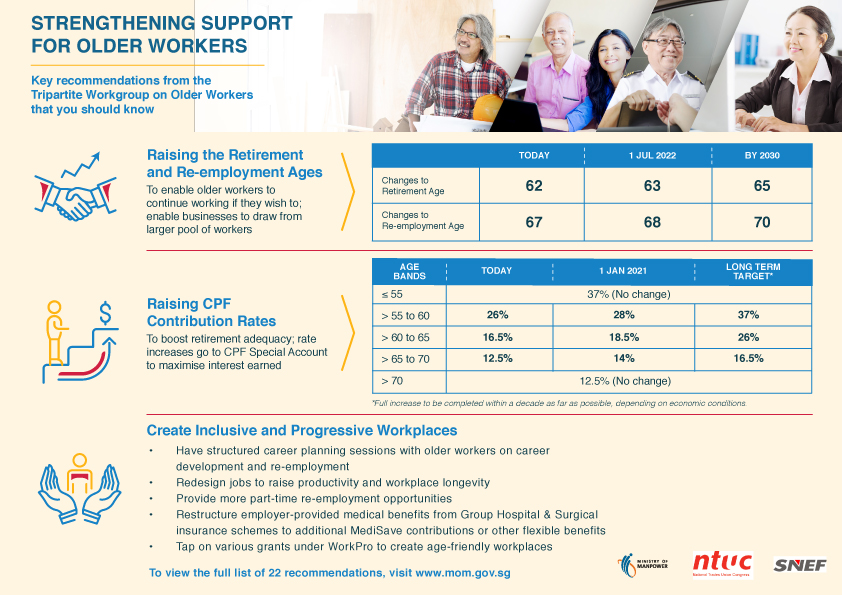

The official retirement age in Singapore is currently 62. But PM Lee Hsien Loong unveiled plans during the 2019 National Day Rally to gradually raise the current official retirement age of 62 to 65 by 2030. It also plans to raise the "re-employment age" -- the age at which employers must offer re-employment to eligible employees -- from 67 to 70 by the same time frame.

Here's what that looks like:

| 2019 | 2022 | By 2030 | |

| Retirement age | 62 | 63 | 65 |

| Re-employment age | 67 | 68 | 70 |

- raise current official retirement age of 62 to 65 by 2030

- re-employment age will be raise from 67 to 70 by the same time frame.

[caption id="attachment_34216" align="alignnone" width="640"] Source: National Day Rally 2019[/caption]

Source: National Day Rally 2019[/caption]

What's the difference between retirement age and re-employment age?

Currently, the minimum retirement age is 62. What that means is that it's against the law for your company to ask you to retire before that, barring of course, grounds for dismissal under poor performance. Of course, you can choose to retire anytime you want. Those who want to continue working beyond the age of 62 can also seek for re-employment with their existing employer.

Under Ministry of Manpower guidelines, employers must offer re-employment to eligible employees who want to continue working up to the age of 67 within their company. You are eligible for re-employment if you:

- Are a Singapore citizen or permanent resident

- Have served your current employer for at least 3 years before turning 62

- Are medically fit to continue working

- Have satisfactory work performance

Changes to CPF contribution rates

While the official retirement age is gradually being raised, CPF contributions for older workers are also being raised to make it attractive for them to stay employed. From the year 2021, CPF contribution rates for workers above 55 will be raised gradually until 2030.

Here's what that looks like:

Note: There will be no change to CPF withdrawal ages, which remains at 55 years old. Upon reaching 55 years old, members can withdraw up to $5,000 from their Special and Ordinary Accounts, or anything above their Full Retirement Sum (FRS) in their Retirement Account (RA), whichever is higher.

Don't Think of Retirement as a Fixed Number

But does that mean you can't retire before the current age of 62? Of course not. You can stop work anytime you want, provided you can still sustain your means of living and that of your dependants. Conversely, there are people who are also past the age of 62 now, who still want to work.

There are two, more realistic ways to determine the "right" retirement age.

1) Base retirement on how much savings you have

This is the soundest way to decide when to retire: by not using your age, but your savings. After all, if you have a S$10 million by age 30, then you can probably quit working right there and then, because you are no longer salary- dependent. Does it mean you should "retire" and stop working? No, of course not -- what will you do with all that spare time?

Another way to think of it is this: you can "retire" and work because you want to, not because you have to. Billionaire Warren Buffet is 88 years old at the time we write this; he still works, but it’s certainly not because he needs the money.

To work out your “retirement age” this way, you need to calculate your desired Income Replacement Rate (IRR). This is the percentage of your current income, which you want to have when you’re retired.

For example, say you earn S$60,000 per annum. As a rule of thumb, you need to retire with an IRR of about 70 per cent, to maintain more or less the same standard of living. In this case, that would mean a post-retirement income of S$42,000 per annum.

Once you have this figure, you can work out how much you need to last till the age of 90. In the above example, say you manage to amass S$1.26 million, by the age of 60 (through investing, downsizing your house, saving a lot, etc). In such a case, you’d have S$42,000 per annum until you’re 90, and it could be viable to retire at that point.

(But note the S$1.26 million also needs to be invested in a way that grows at three to five per cent per annum, to keep up with inflation. Speak to a financial advisor for more details).

What's your desired lifestyle?

Note that, if you’re happy to live a more spartan lifestyle, this also means you can retire earlier. For example, say you earn S$60,000 per annum, but are happy to live a simple life (no overseas vacations, simple meals at home or at coffeeshop.) You just need an IRR of 50 per cent.

In such a case, you could retire as early as around 52: you’d only need S$30,000 per annum, so you just need S$1.14 million; less than the S$1.26 million you’ve already saved.

You could also try to be more ambitious. For example, some people aim to have a 100 per cent IRR. Let’s say you run your own business, to get an income of S$60,000 a year. You could then pick the retirement age of 70, after which your S$1.26 million could provide the full S$60,000 a year, until you’re age 90.

By thinking of your retirement as a number, rather than a fixed age, it’s easier to plan for the lifestyle you want. The “correct” retirement age is thus dependent on how you want to live.

2) You may have no choice but to stop working

You may not have a say in when you retire. Sometimes, life events such as stroke, progressive disease or a terminal illness dictate when you stop work. While tragic, these are not impossible to prepare for.

It’s important to be well covered by a life insurance policy, with sufficient payouts in such situations. Never plan to work till a specific retirement age, and then simply assume life will take care of you from there.

Besides life insurance, there’s another way to prepare for a forced retirement: alternative income streams. Money from stock dividends, bonds, rental properties or investments in businesses are all forms of passive income. They can continue to provide money, even if you’re forced to stop working.

As such, it’s important to invest and build up such assets, while you’re healthy and able.

Retirement thus comes down to three things: comprehensive insurance, passive income streams, and a certain amount of accumulated wealth. It would pay to think of your correct “retirement age” along those parameters, rather than as a fixed age.

Read This Next:

4 Safest Ways to Grow Your Retirement Nest Egg in Singapore

Can You Afford to Retire at Age 50 in Singapore?

By Ryan Ong

Ryan has been writing about finance for the last 10 years. He also has his fingers in a lot of other pies, having written for publications such as Men's Health, Her World, Esquire, and Yahoo! Finance.

Similar articles

Pros And Cons Of Keeping Your Savings In Your CPF Special Account

3 Myths About Retirement Planning in Singapore (And Why They’re Wrong)

Will I Ever Retire in Singapore?

Can You Afford to Retire at Age 50 in Singapore?

What Are You Doing to Plan For Your Retirement?

Retirement Planning - Is CPF Life sufficient and What’s Considered “Enough”?

4 Best Places to Keep Your Retirement Savings in Singapore

What SAF Retirees Should Do With Their Retirement Payouts

Back to Blog

Back to Blog

-2.png?width=280&name=Insurance%20(2)-2.png)

{kind=link}

{kind=link}