Singaporeans with monthly incomes up to S$8,000 are receiving higher contributions in their CPF accounts, which means lower take home pay, but higher Ordinary Account (OA) balances for mortgages. Should these homeowners purchase a larger property using their CPF funds?

CPF salary ceilings are being progressively raised till 2026, where the ordinary wage ceiling will reach S$8,000 per month. This is a significant increase from the previous salary ceiling, which was S$6,000.

One consequence of this change is that those affected will see larger sums going into their CPF accounts, including their Ordinary Account (OA). As OA savings can be used to pay for home mortgages, you may be wondering if you should go for a larger home.

Before you do. It’s prudent to plan your finances properly given that buying a home is a significant financial commitment, with mortgages typically lasting several years or decades.

Also, home loan interest rates are at their highest in the past five years, and are unlikely to come down anytime soon, adding further weight to your decision.

Table of contents:

- Should you use your OA funds to pay for a larger property?

- Things to consider when planning for a larger home

- Find more helpful tools at DBS Home Marketplace

Should you use your OA funds to pay for a larger property?

While one of the purposes of CPF is to help Singaporeans with housing affordability, it is also meant to help meet retirement needs. Spending more of your CPF funds on housing means you will eventually have a smaller sum going into your CPF Life account, which means you’ll get small monthly payouts in retirement.

However, if you use your CPF OA to purchase a larger property, you may benefit from higher capital appreciation should your type of property happen to be in hot demand. Upgrading to a larger home also means more rooms that you can rent out, translating to higher rental income to fund your retirement needs.

On the other hand, if you choose to invest your CPF OA balance, or let it compound at the guaranteed interest rate, the increased monthly contributions will help you build your retirement nest egg at a faster pace. But this would mean you’ll need to foot your mortgage from your take home pay, leaving you with a smaller cash budget each month.

Things to consider when planning for a larger home

Determine how much you can afford to spend on your home

You can check your CPF statement to see how much is deposited into your OA every month. This will tell you how much you can spend each month on mortgage payments, which should not exceed 30% of your gross monthly income. So how large a mortgage can you take? And over how many years?

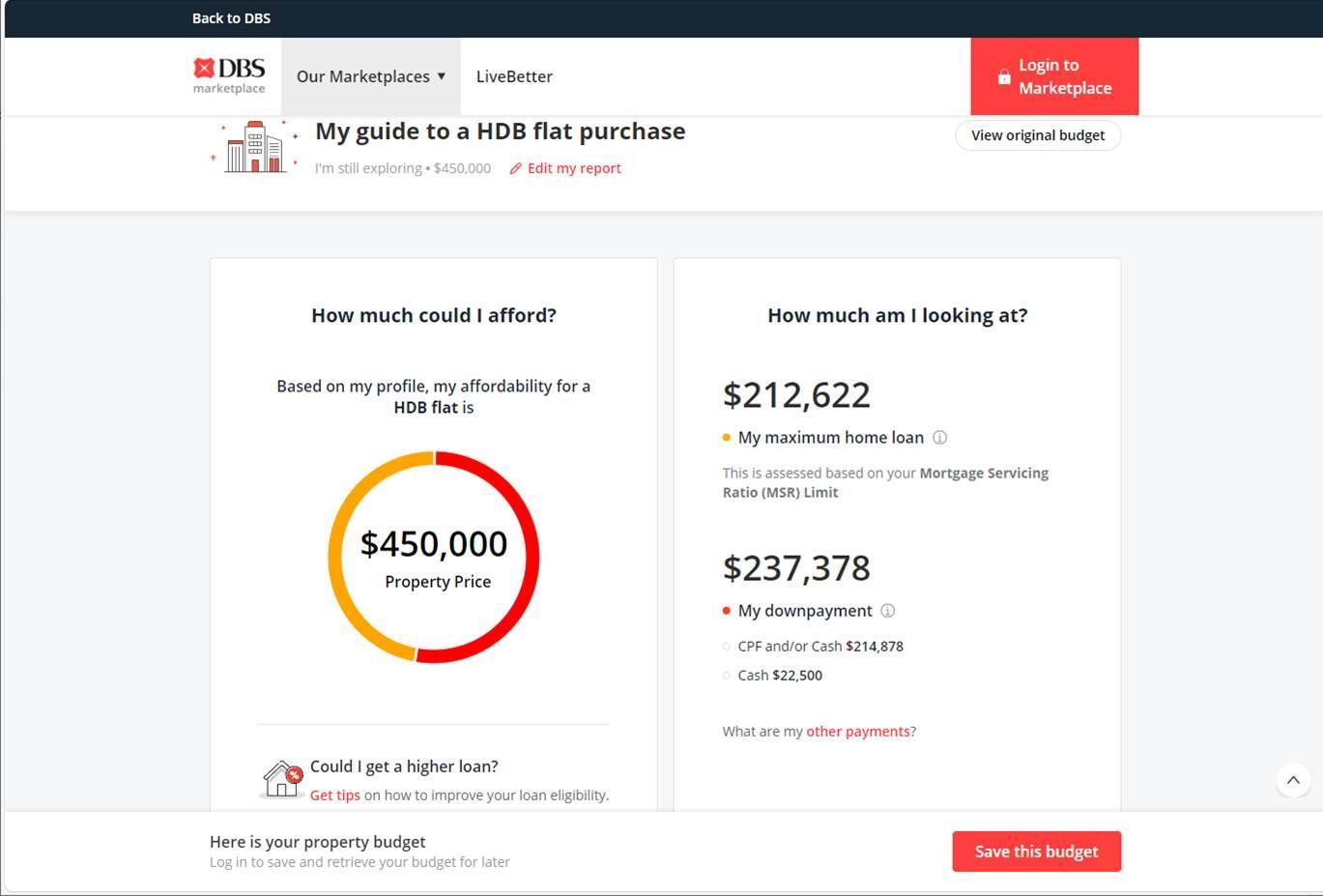

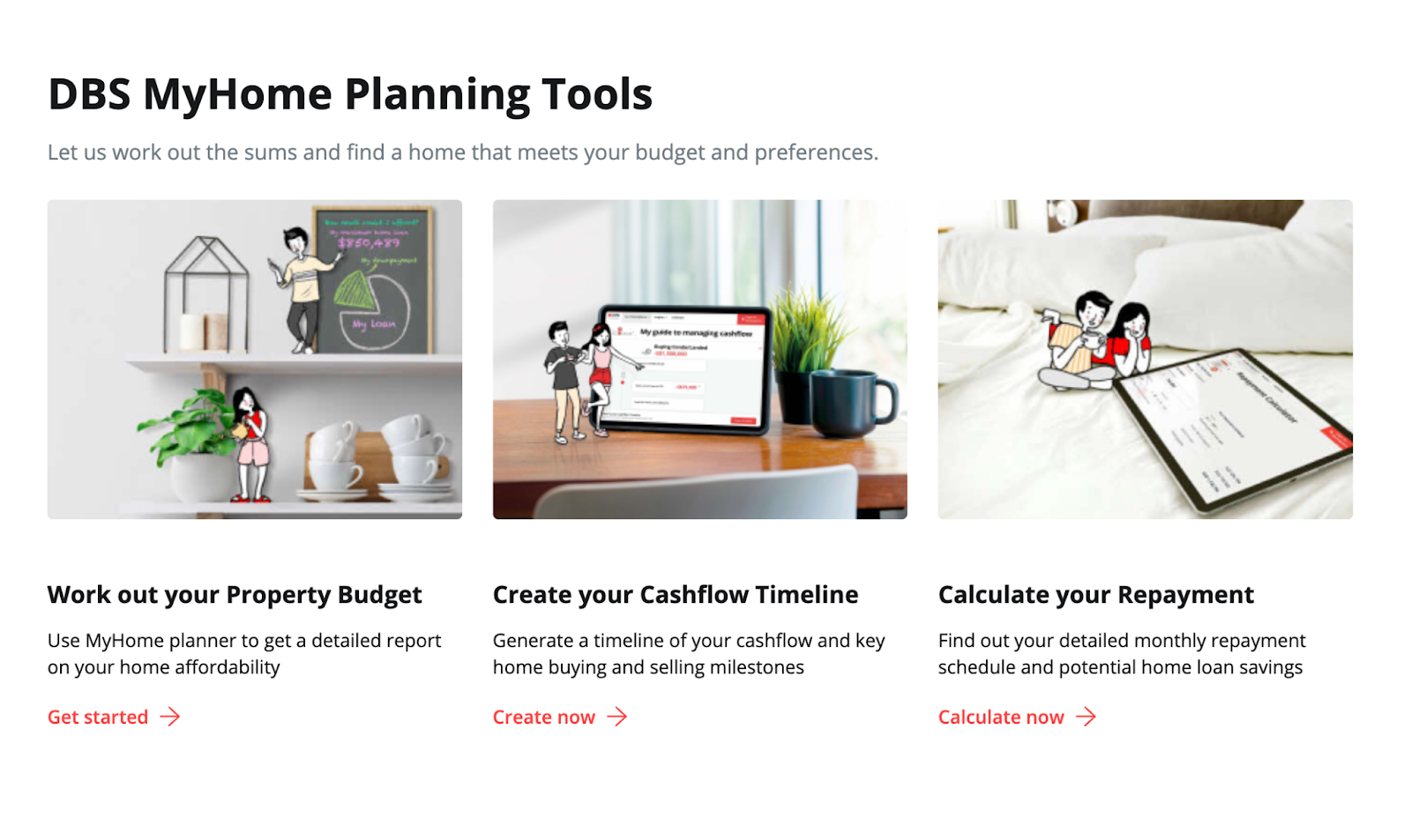

A quick and easy way to find out is to use DBS MyHome Planner, a free online mortgage planning calculator.

All you have to do is to answer a few simple questions on your salary, existing debt payments, residential status and type of property, and a personalised home affordability report will be generated for you.

Some key data points provided include:

- How much you can afford to spend on a home

- Your maximum mortgage amount

- Your downpayment

- Monthly instalment amounts across different loan tenues (5 to 20 years)

Armed with this information, you’ll have a clearer idea of how large a home you can afford with your increased OA contributions.

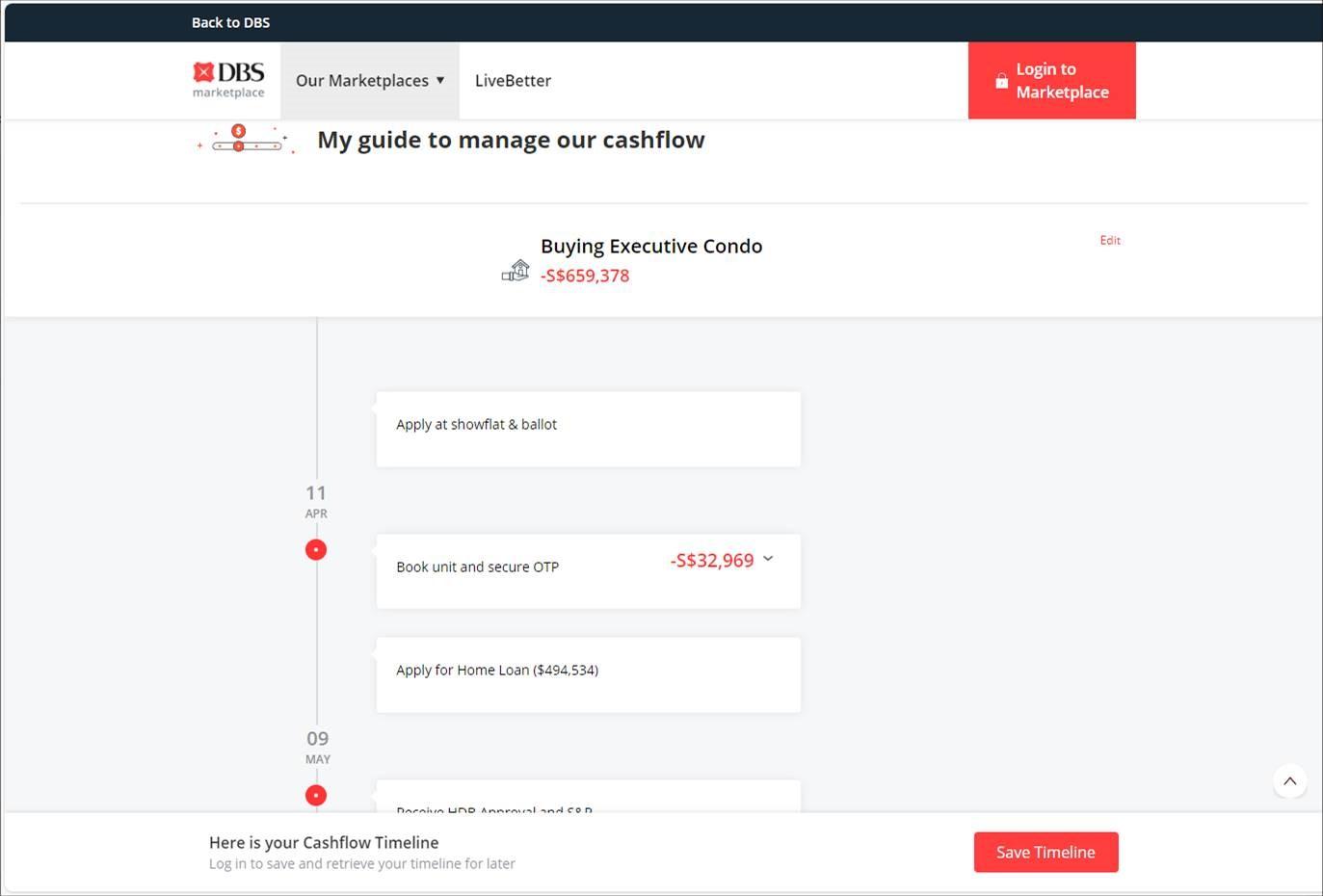

Have a payment timeline

In the process of upgrading to a larger property, you’d need to make several different payments before starting your mortgage. Having a timeline is helpful in visualising your cashflow so you can be better prepared.

Try out the Cashflow Timeline, which is another tool offered under the DBS Home Marketplace. Simply answer a few questions, and a personalised timeline will be generated for you. Refer to it to know when you’d need to make certain payments, and how much to pay.

Look for the best mortgage rates

Getting the lowest interest rate on your mortgage is crucial. This is because given the high principal sum involved, even a small difference in rates will add up to a significant sum in the end.

The Repayment Calculator is a handy tool for working out the total interest paid under the terms of your mortgage. It shows you this clearly in a repayment schedule, and you can input different interest rates to see the difference in dollar terms, so you can make an informed decision.

Find more helpful tools at DBS Home Marketplace

The increase in CPF OA contributions represents an opportunity for some homeowners to upgrade to larger properties. But this is a significant financial endeavour that merits proper planning and forecasting for the best possible outcome.

That’s where financial planning tools like MyHome Planner, Cashflow Timeline and Repayment Calculator come into play. Try them out and you’ll be surprised at how much clearer things become.

Additionally, you can also compare attractive home and renovation loans, get insurance coverage for your home contents via myHome Protect II, and find more helpful tools and resources over at the DBS Home Marketplace.

From renovation and utilities (electricity, broadband, mobile) offers, to guides and articles on home ownership, you’ll find everything you need to help you attain your dream home.

This article was written in partnership with DBS.

Disclaimers

myHome Protect II is underwritten by Chubb Insurance Singapore Limited (“Chubb”) and distributed by DBS Bank Ltd (“DBS”). It is not an obligation of, deposit in or guaranteed by DBS. This is not a contract of insurance. Full details of the terms, conditions and exclusions of the insurance are provided in the policy wordings and will be sent to you upon acceptance of your application by Chubb.

You have a free look period of 30 days from the date you receive the Policy. If you decide to cancel the Policy within these 30 days, please inform Chubb in writing and they will cancel the Policy from its start date and refund the full premium paid, provided no claim has arisen.

This policy is protected under the Policy Owners’ Protection Scheme which is administered by the Singapore Deposit Insurance Corporation ("SDIC"). Coverage for your policy is automatic and no further action is required from you. For more information on the types of benefits that are covered under the scheme as well as the limits of coverage, where applicable, please contact Chubb or visit the HYPERLINK "http://www.gia.org.sg" General Insurance Association or HYPERLINK "https://www.sdic.org.sg" SDIC websites.

Similar articles

What is Legacy Planning, and When Should You Start?

School Didn’t Teach Me: Money Lessons I’ve Learnt After Moving In With My Partner

Should You Always Pay Your HDB Downpayment With Cash Or CPF?

6 Things That SG Couples Regret Spending On Their Weddings (And The #1 Thing They Don’t)

Zig Rewards vs GrabRewards – Which Offers You Better Rebates?

Credit Card Comparison: POSB Everyday vs Citi Cash Back vs OCBC 365

8 YouTubers To Follow For Home Workouts (HIIT, Yoga, Cardio And More)

How to Buy Your First Investment Timepiece (And Why You Should)

Back to Blog

Back to Blog