If you know how you’d prefer your assets to be distributed when you pass on, it’s best to do some legacy planning, rather than have it distributed according to Singapore’s intestacy laws. Here’s a guide to leaving a legacy in Singapore.

When you pass on, your loved ones might no longer have the income that you bring home. However, the bills they have to pay are likely to remain the same. By leaving behind a legacy that is distributed the way you want it to, you can safeguard them financially even when you’re not around.

Here’s how you can plan to leave a legacy in Singapore.

What does leaving a legacy mean?

Leaving a legacy refers to distributing the assets and possessions that you eventually leave behind when you pass, according to your wishes. These assets can include cash, investments, property, insurance cash value and your CPF.

As life is unpredictable, planning to leave a legacy shouldn’t just come only towards the end of your life. You can start planning for it even as you plan for your retirement, before you lose the mental capacity to make a decision that best reflects your intentions.

Why is leaving a legacy important?

Planning to leave a legacy allows you to make a lasting impact on the people that you leave behind, as well as the generations to come.

It is also one way that you can help to bring up and protect your loved ones even when you leave. This could mean providing your children with the financial support to attend university, or simply for your family to be financially comfortable even when you’re gone.

On a personal level, it also ensures that all the hard work you’ve put in during your lifetime towards accumulating these assets are not gone to waste, being distributed according to your wishes.

Ready to level up? Find out how you can make your money work harder and smarter for you. Enjoy your own dedicated relationship manager and privileged access to a whole suite of preferential rates with Priority Banking. Compare your options.

How do I leave behind a legacy in Singapore?

#1 List down all your assets

Firstly, you should list down everything you own under your name. This not only helps you to ensure that nothing is left out as you plan your legacy, it will also help to ensure that your loved ones know where all your assets are at.

A few of the common assets include:

- Property: All the details and information you have surrounding the property you own, including details of the home loan. However, do keep in mind that property under joint tenancy will have the ownership passed on to the remaining (surviving) joint owner.

- Cash: Round up all the cash that you have. This could be physical notes, cash in your savings account, fixed deposits and other avenues.

- Investments: Gather all your investment accounts, such as your robo-advisor portfolios, brokerage accounts, forex accounts, bonds and all the securities you hold in your Central Depository (CDP) account. You should also keep a record of the login details to the various investment accounts you have.

- Insurance plans: This should include investment plans, endowment plans, life insurance, any other savings plans and more. While you can nominate beneficiaries for your life insurance plan, there is also no harm listing down your life insurance plans within your will.

- CPF: Note down how much you have in all your CPF accounts — Ordinary Account (OA), Special Account (SA), MediSave account (MA) and Retirement Account (RA).

- Valuable possessions: Such as jewellery, antiques, furnitures and pieces of art

#2 Decide how you would like your assets to be distributed

Do you want to leave it all to your spouse? To your children? To your parents and siblings? Or would you like to donate a portion of your wealth to those in need?

Besides choosing who to receive your assets, you would also need to decide on the percentage each recipient would receive.

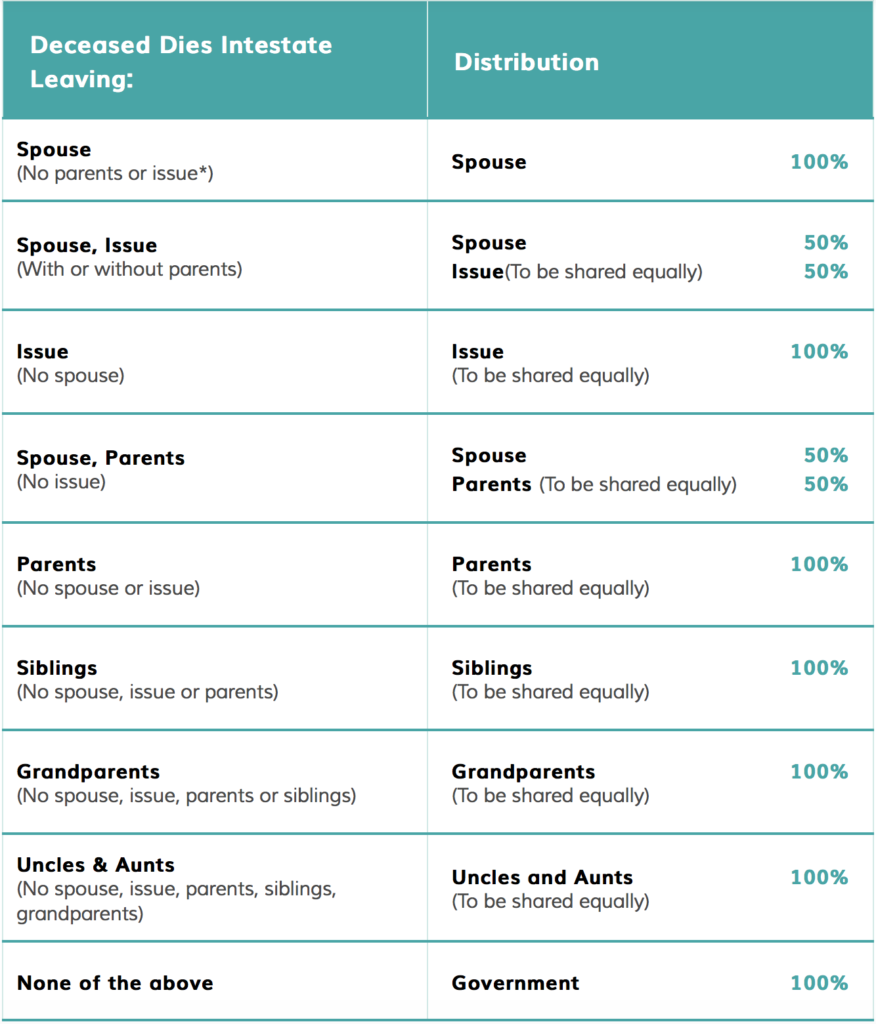

Here’s a simplified version of how your assets will be distributed, if left to the Intestate Succession Act.

*Issue includes children and the descendants of deceased children.

#3 Write a will

The key component of leaving a legacy is to write a will.

If you don’t write a will, your assets will be distributed according to Singapore’s intestacy laws — this might not be ideal or according to how you’d most prefer. A will can also help to avoid any potential disputes or lawsuits over the inheritance, and also reduce any potential delays in terms of distribution.

Your will should contain the details of all the assets that you have, including information on how you want the assets to be distributed, managed and transferred to the people that you leave behind.

In case you think that writing a will is a tedious process that requires money and the services of a lawyer, today, there are platforms that you can tap on to write a will completely digitally.

To help you out, MoneyOwl offers a free, online will writing service that takes just 10 minutes to complete.

Is a will all I need?

Besides writing a will, when planning your legacy, you should also consider doing the following, as not all assets can be distributed via a will.

- Make a CPF nomination

Your CPF money cannot be covered under a will, as they are excluded from your estate. Hence, you’re strongly encouraged to make a CPF nomination.

A CPF nomination will allow you to specify who will inherit your CPF savings, the percentage they receive, as well as how the savings will be distributed (by default, your nominees will receive the CPF savings in cash via cheque or GIRO). Your CPF savings include the money in your CPF OA, SA, MA, RA and your CPF LIFE premium balance.

If you don’t make a nomination, your CPF money will instead be distributed by the Public Trustee’s Office (PTO) to the legally entitled beneficiaries, Intestate Succession Act or the Inheritance Certificate (for Muslims).

Making a CPF nomination is free of charge and can be done online. All CPF members can make CPF nominations as long as you’re aged 16 and above. This means you can make the nomination as soon as you start growing the money in your CPF accounts. Here’s the link to help you get started.

- Nominate beneficiary for insurance

You should also nominate beneficiaries for your insurance policies — particularly the ones with death benefits. The beneficiaries will receive the proceeds and payouts of your insurance plans when you pass on. Do note an irrevocable nomination cannot be overridden by a will.

Making a nomination for your insurance plans also helps to ensure that the payouts will be distributed sooner, potentially helping to alleviate the immediate expenses upon death. If you don’t nominate a beneficiary, the insurance payouts will be distributed according to your will, or in accordance with the Intestate Succession Act.

Read more about nominating beneficiaries for your insurance plans.

Whether you’re planning your legacy starting today, or in the years to come, as you continue to amass your assets, you can also consider opening a priority banking account to supercharge your wealth. A priority banking account can put your current assets to good use, helping you unlock exclusive perks, including having a personalised relationship manager to help you grow your wealth.

Read these next:

9 Things To Do With Your Inheritance Money In Singapore

CPF Nominations: What Happens To Your CPF Money After You Die?

Why You Should Nominate Beneficiaries For Your Insurance Policies & How To Nominate

Being Rich vs Having Wealth: What’s The Difference

CPF Special Account (SA) Shielding: How You Can Perform This Retirement ‘Cheat Code’

Similar articles

Inheritance Planning: 5 Important Things You Should Know

What is Legacy Planning, and When Should You Start?

Not Ju$t You: Someone Needs to Know Where Your Money Is

What is Will Writing and How Does That Impact Your Legacy Planning?

Estate Planning for Women 101 – 5 Key Things to Know

Why You Should Nominate Beneficiaries For Your Insurance Policies & How To Nominate

The Real Cost: Will Writing — How Much It Costs, Where To Go, And more

CPF Nominations: What Happens To Your CPF Money After You Die?

Back to Blog

Back to Blog

-2.png?width=280&name=Insurance%20(2)-2.png)