Flexibility is a crucial trait to have, especially for everyone who’s navigating through the new norm.

Among insurance products, investment-linked policies (ILPs) offer coverage that a traditional life insurance policy has, protecting you against events such as death and total and permanent disability (TPD). They also feature an investment component that potentially grows your money. This is accomplished when you determine which investment-linked fund(s) your insurance premiums go towards.

When combined, these factors make ILPs an excellent complement to both your suite of investments and insurance plans. However, ILPs have developed a poor reputation through the years for two reasons:

- They are admittedly complex financial instruments due to their multiple components and non-guaranteed returns.

- Some financial advisors push these policies onto customers who might not know any better.

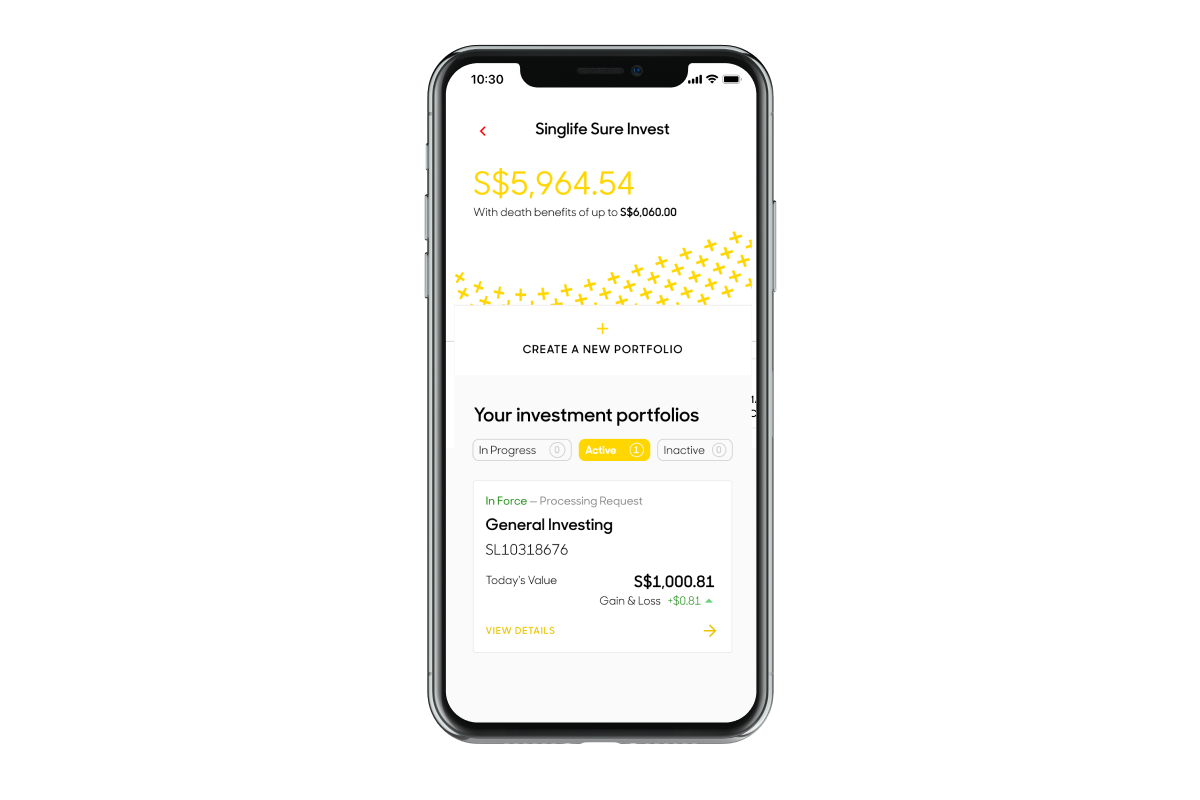

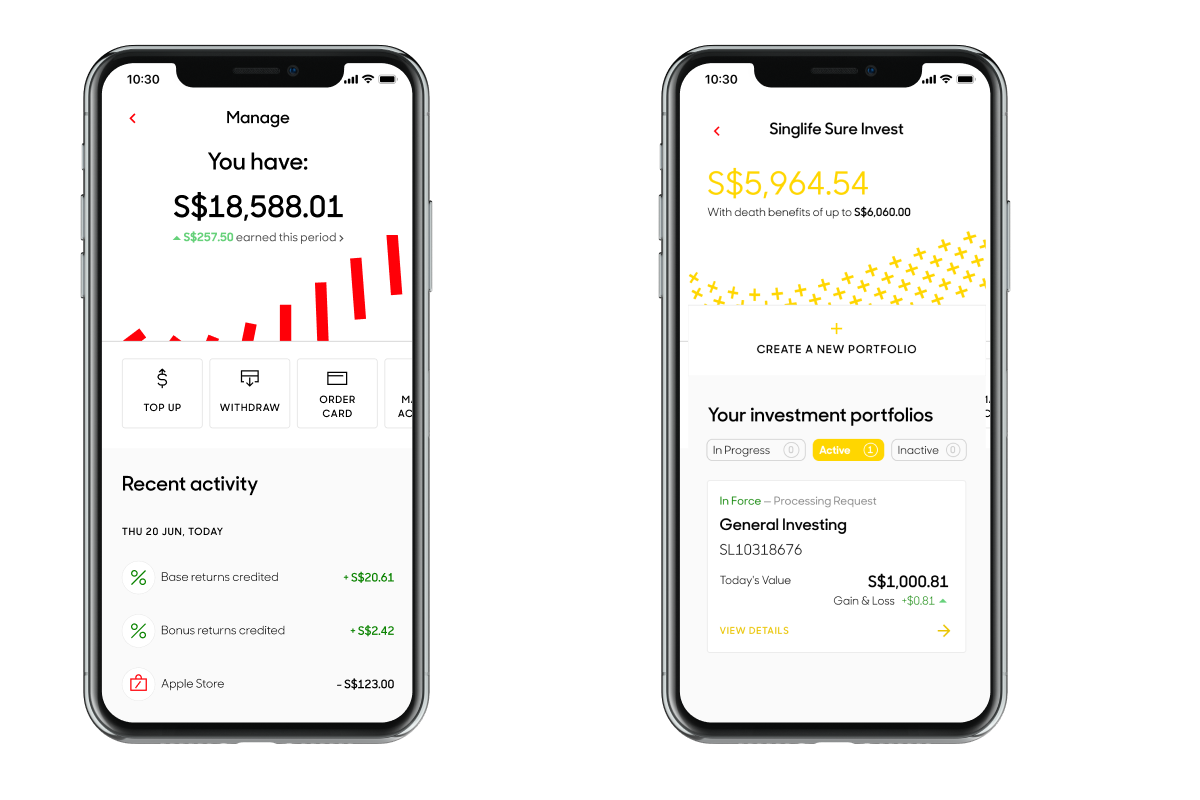

Singlife’s latest product, a digital ILP dubbed Sure Invest (you can access it via the Singlife app), is set to change your perception of ILPs altogether.

1. Greater Transparency

Traditional ILPs typically offer a comprehensive performance report regarding their underlying funds just once every six months. This is in stark contrast with other investments that allow you to access performance data at any time, such as stocks and robo-advisors.

Singlife’s Sure Invest functions exactly as such due to its app-based nature. You’re given access to your policy’s performance 24/7 without skimping on the level of detail that a traditional ILP’s report offers, all in a single page.

Also, you only pay a single management charge of 0.25% of your account per calendar quarter. There are no other fees that threaten to eat into your returns. This means there are none of the frilly and oftentimes hidden charges like sales charges, admin charges or surrender charges that people lament about in ILPs.

Ditto for the premiums paid, with 100% being invested to purchase units in Sure Invest’s investment-linked funds.

2. Greater Accessibility

As Sure Invest sits alongside your Singlife Account, accessing it is a breeze. You can create a new portfolio, customise your current ones, invest, or make a withdrawal in just a few taps. The integration between your Singlife Account and Sure Invest means that transfers are fuss-free too.

For budding investors or individuals with heavy financial commitments, Sure Invest grants you the opportunity to invest at your own pace. Here’s why:

- There aren’t any no lock-in periods or withdrawal fees, giving you peace of mind and a high level of liquidity. The no lock-in feature has been touted as one of the biggest draws of Singlife’s mobile products in general, and investors know it.

- You can choose to contribute on an ad-hoc or monthly basis starting from $100 after the initial single premium of $1,000 has been paid.

Even the portfolios you can invest in have been boiled down to just three, catering to individuals with different risk tolerance levels. No longer do you need to endure the choice paralysis of choosing from a variety of sub-funds that might need to be rebalanced regularly.

You can now leave the portfolio allocation and rebalancing to the experts at Aberdeen Standard Investments, who are world-renowned fund managers. Also, you aren’t required to stick with a single solution since you can create multiple portfolios. You can also switch your portfolio at any time. Neat, right?

Here are more details regarding Singlife’s portfolios1.

| Portfolio | Singlife Conservative | Singlife Balanced | Singlife Dynamic |

| Asset Allocation | 80% Fixed Income: Global Investment Grade Bonds, Singapore Short Term Bonds, US High Yield Bond Fund, Asian High Yield Bond Fund 20% Equities: Global Equities, Asia Pacific Ex Japan Equities |

50% Fixed Income: Global Investment Grade Bonds, US High Yield Bond Fund, Asian High Yield Bond Fund 50% Equities: Global Equities, Asia Pacific Ex Japan Equities, Global Equities Low Volatility |

20% Fixed Income: Global Investment Grade Bonds, US High Yield Bond Fund, Asian High Yield Bond Fund 80% Equities: Global Equities, Asia Pacific Ex Japan Equities, Global Equities Low Volatility |

| Risk Level | Low | Medium | High |

| Volatility Tolerance | Low | Medium | High |

| Performance (29/7/2020- 31/12/2020) |

+5.83% | +8.34% | +10.28% |

Although these portfolios have varying asset allocations and risk levels, they are all designed with one goal in mind: to help you achieve long term growth.

If you have a look at their factsheet here, what you’ll be able to glean about the portfolios are as follows:

3. Greater Flexibility

| Singlife’s Sure Invest | Features Common To Traditional ILPs |

| Lock-in period: None | Lock-in period: 5 -10 years |

| Surrender charges: $0 | Surrender charges: Ranges from 1 -10% of policy value |

| Withdrawal fee: $0 | Withdrawal fee: Max. 5% of policy value |

Sure Invest has much greater flexibility compared to other ILPs in the market, not having the lock-in periods or surrender charges that other policies might have. If you decide that a portfolio isn’t meeting your financial goals, you don’t have to worry about being penalised unfairly or missing out on another investment opportunity.

Being able to make a withdrawal at any time with no fees levied makes Sure Invest an apt investment for younger working professionals who might not be financially secure. Should there be an emergency that requires immediate funding, you can easily make the withdrawal by transferring the funds to your Singlife Account.

And because you’re able to view your portfolio’s performance regularly, you can decide whether to switch your portfolio or create another one with a different risk level in order to meet your financial goals. It’s akin to the fund-switching of traditional ILPs, but without the cost incurred after using up your allotted number of free switches.

4. Simplified Choices

| Product | Insurance Coverage Value |

| Singlife’s Sure Invest | 101% of net premiums or account value (whichever is higher) |

| Traditional ILP | Varies across providers and plans |

As mentioned earlier, ILPs boast both an investment component and life insurance coverage. Sure Invest is a great way to kickstart your insurance coverage or round out the protection you might already have. Should anything untoward happen, your nominees will always receive 101% of your net premiums or your account value, whichever is higher.

On the other hand, traditional ILPs have varying levels of coverage. Should you decide to increase your coverage, it results in a lower percentage of your premiums being invested in the various sub-funds.

Sure Invest also grants you security via its provider, Singlife. Like all reputable financial institutions in Singapore, Singlife is licensed by the Monetary Authority of Singapore. All assets are held in custodian accounts. This means that if Singlife ceases operations, your investments will not be affected.

A departure from traditional ILPs, Sure Invest is a digital ILP from Singlife, offering insurance coverage and the opportunity to grow your wealth. It’s fully integrated with Singlife’s suite of products, so you can manage your money, invest, and insure yourself via a single app.

Want to know more? Check it out now!

This article is written in partnership with Singlife

1Source: ASI Asia. As at 31/12/2020. The asset class allocation may change from time to time as a result of a change in portfolios allocation, at the discretion of the Asset Manager. Figures may not always sum up to 100% due to rounding.

The table above sets out the gross model performance returns (BEFORE investment manager fees, administration fees, advisory fees and taxes) for the Portfolio. Had such fees been deducted, returns would have been lower. The performance of the model portfolios may differ from the actual portfolios held by the individual investor. The performance returns have been calculated on a daily basis, and are accumulated for the period shown. Performance returns shown are annualised if the period exceeds 1 year, or as total returns otherwise. Past performance is not a guide to future results.

Note that the performance for your Sure Invest portfolio is not guaranteed and the value of the units and the income accrued to the units (if any) may fall or rise. You can choose one of the three risk-levels portfolios per policy.

The information is meant for your general knowledge and does not regard any specific investment objectives, financial situations or particular needs any person might have and should not be relied upon as the provision of financial advice.

Singlife’s Sure Invest is an Investment-Linked Policy (ILP) that invests in the respective ILP sub-funds within your chosen portfolio. Investment products are subject to investment risks including the possible loss of the principal amount invested. The portfolio performance is not guaranteed and the value of the units and the income accruing to the units (if any) may fall or rise. Past performance is not necessarily indicative of future performance.

A product summary, terms and conditions and factsheet relating to Singlife’s Sure Invest are available. You should read the product summary, terms and conditions and fact sheet before making a commitment to purchase Singlife’s Sure Invest is protected under the Policy Owners’ Protection Scheme which is administered by the Singapore Deposit Insurance Corporation (SDIC).

Coverage for your policy is automatic and no further action is required from you. For more information on the types of benefits that are covered under the scheme as well as the limits of coverage, where applicable, please contact Singlife or visit the LIA or SDIC websites (www.lia.org.sg or www.sdic.org.sg).

This advertisement has not been reviewed by the Monetary Authority of Singapore.

Information first published on 13 March 2021, with updates on 27 June 2022

Read these next:

Guide To Investment-Linked Policies (ILP): What You Need To Know

5 Best Sustainable Investments In Singapore

Insurance Savings Plans: Singlife Account vs GIGANTIQ vs SingTel Dash EasyEarn

5 Tips For Millennials To Start Adulting Financially

4 Investing Tips I Learnt The Hard Way That All Beginners Should Know

Similar articles

Money Confessions: 9 Singaporeans Share Their Portfolio Asset Allocation

Guide To Investment-Linked Policies (ILP): What You Need To Know

6 Ways An Investment-Linked Policy Can Play a Part in Your Recession-Proof Strategy

Got $50? Here Are 3 Easy Investments To Start Growing Your Money (And 1 To Avoid)

What Place Do ILPs Have In Your Wealth Accumulation Strategy?

This Is How Par Policies’ Reduced Illustrative Rate Of Returns Affects You

Grab Launches GrabFin To Unify Its Financial Services, Introduces New Investment Service Earn+

Buy Term, Invest the Rest (BTIR): The Complete Pros And Cons Breakdown

Back to Blog

Back to Blog