FIRE has become a buzzword through the years. Find out how you can build up a six-digit net worth by the time you hit the big three-o.

By now, you should have heard about FIRE (Financial Independence, Retire Early). It is a lifestyle movement that seeks to maximise your savings rate and investment returns to achieve the goal of financial independence at a younger age.

Upon reaching financial independence, FIRE followers can decide to continue working, scale back to part-time work, or simply retire early. The choice is yours.

On the road to FIRE, one of the milestones among FIRE followers is to build a net worth of S$100,000 by the age of 30. According to a Credit Suisse report, the median net worth among Singaporeans is US$86,717 (approximately S$117,000).

Can a 30-year-old achieve a net worth close to the national median a few years out of school? Let’s find out.

First, let’s make a few assumptions:

- Singaporean women typically graduate from university at age 22, but Singaporean men graduate later at age 24 (due to National Service). Thus, Singaporean men only have six years of work before they hit age 30. We will therefore use six years as the base scenario.

- The individual starts working immediately after graduation.

- The median gross monthly salary for university graduates in Singapore is S$3,700. Including employer CPF contributions, the individual contributes 37% of their gross salary (i.e., S$1,369) to CPF. He spends the rest, and his salary remains stagnant.

- The individual is not buying a property before age 30 (to simplify net worth calculations).

- The individual has no savings, debt, or commitments (starting from ground zero).

I understand the above assumptions may not apply to every personal situation, but I believe they hold true for many Singaporeans. Most of us live with our parents before marriage (enabling us to save more money), and we typically only buy a home after marriage.

The average age for marriage in Singapore is also around 30 for both men and women, so this lines up perfectly with our assumptions.

In the scenario above, the individual only contributes to CPF and doesn’t save any of his take-home pay (although he should, by the way). Can he still hit a net worth of S$100,000 within six years by age 30?

Let’s calculate this. Here are the steps:

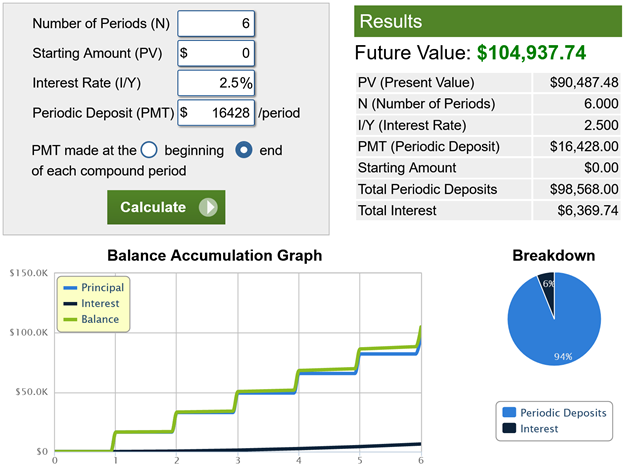

- S$1,369 x 12 months = S$16,428 in annual contributions

- The interest rate for the CPF Ordinary Account is 2.5% per annum

- Compound S$16,428 in annual contributions at 2.5% p.a. for six years

What will you accumulate after six years?

As you can see, just relying on his CPF contributions alone, growing at 2.5% p.a., will enable the typical Singaporean university graduate to reach a net worth of S$105,000 by age 30.

In reality, this amount will be slightly higher as CPF interest is computed monthly, and you also earn a higher interest rate (4% p.a.) for money in your CPF Special and Medisave Accounts. But, of course, the caveat is that you can only withdraw your CPF money at age 65.

Quarter-millionaire by 30?

Since the goal of reaching S$100,000 by 30 is quite achievable, how about a more ambitious goal? Can a typical Singaporean university graduate hit S$250,000 by 30? To do that, you’ll need to save some of your take-home pay and start investing.

Here’s how to do it:

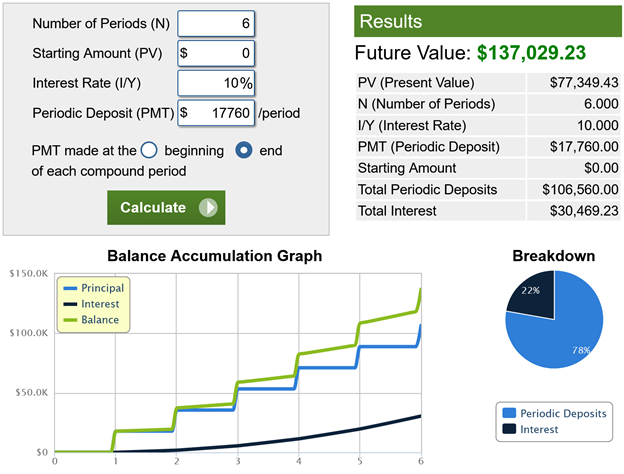

- After your CPF contributions, your monthly take-home pay is SS$2,960. Save half of your take-home pay (i.e., SS$1,480). SS$1,480 x 12 months = SS$17,760 in annual savings.

- Invest your savings in an exchange traded fund that tracks a broad-based market index like the SPDR S&P 500 ETF Trust (SPY). The long-term annualised return of the SPY is about 10%.

- Invest SS$17,760 annually at 10% p.a. for six years

How much will your investment grow after six years?

Coupled with additional savings and investing in the stock market, an individual can accumulate an additional S$137,000 by the age of 30. Add that to the money in your CPF, and you would have a net worth of S$242,000, close enough to our goal of a quarter million. With that financial base by your 30s, you’re well on your way to FIRE.

However, there are some important considerations to note.

Investing in the stock market introduces risk. On the other hand, saving money in your CPF is essentially risk free; you can be sure that you will receive 2.5% to 4% in interest every year.

While the S&P 500 has grown 10% p.a. on average historically, past results are not indicative of future performance. You also have to note that the stock market doesn’t go up in a straight line; the market can be very volatile in the short term.

The perfect example of this was during the pandemic when markets around the world crashed; the S&P 500 plunged by more than 30% from February to March 2020.

It’s important to keep a long-term perspective when the stock market falls and not be swept away by your emotions. For example, if you had panicked back in March 2020 and sold your investments then, you would have taken a massive hit to your net worth.

Remember, the overall stock market tends to rise over time, so buy and hold if investing in an index ETF is your long-term strategy. However, this strategy only applies to investing in the stock market as a whole; individual companies have no assurance that they will always remain successful.

Final thoughts

FIRE follower or not, financial independence and retirement planning should be key objectives for everyone. And at the core of any successful financial strategy is the concept of saving.

The examples above show how an individual can only reach a six-figure net worth by 30 if he saves enough to invest. Without any savings, you have nothing to grow your money.

Are you well on your way to S$100,000 by 30? If you are, congratulations! And even if you’re not, don’t worry. The best time to start planning for your financial independence is always right now.

“The best time to plant a tree was 20 years ago. The second best time is now.”

Read these next:

Beginner’s Guide To CPF Retirement Sums And How To Get There (2021)

How To Calculate Your Net Worth In Singapore?

All You Need To Know About Income Tax In Singapore

Financial Independence vs Financial Freedom: What Are You Looking For?

Regular Savings Plan (RSP): What They Are And The Best Ones To Invest In

Similar articles

Are Robo Advisors Worth It? Here’s How To Decide

How to Use Personal Loans to Protect Your Cash

Retiring Early: Why The F.I.R.E Movement Might Not Work For Everyone

What is The Average Salary in Singapore And Are You Earning Enough?

How To Calculate Your Net Worth In Singapore?

The Best Investment Strategies to Apply At Each Decade of Your Life

Gender Investing Gap – Should Women Invest Differently?

Is It Possible To Attain Financial Freedom Without Investing?

Back to Blog

Back to Blog