Are earning miles through online payment platforms worth the admin fee? That depends on how you value a mile.

Opinions expressed reflect the view of the writer (this is his story).

It’s tax season once again, and all good, law-abiding citizens will have completed and submitted your income tax returns (Form B/B1) by now.

All that’s left to do is wait for the Notice of Assessment (NOA) to arrive, sign up for a GIRO plan and render to Caesar each month. Move along now, no opportunities to earn miles here.

Or are there?

Although it’s not possible to pay income tax directly to IRAS with a credit card, there are numerous ways to achieve the same end by paying a small admin fee.

Let’s explore how you can earn miles by paying taxes with your credit card, and more importantly, whether it’s worth the admin fee charged.

What Are My Options for Paying Income Tax?

There are two main ways of paying IRAS with a credit card: bank payment facilities and third party facilities.

Bank payment facilities are offered by HSBC, Standard Chartered, DBS, Bank of China, OCBC, and UOB.

Third-party facilities include CardUp, ipaymy and Citi PayAll*. Here’s an example of how to pay your income tax through CardUp.

*Citi PayAll is a service provided by Citibank. However, its mechanism is similar to a third party payment provider, so I’ve classified it along with third party options. More on this below.

Here’s how these options measure up.

| Bank Facilities | CardUp | ipaymy | Citi PayAll | |

| Payment Mechanism | Funds deposited in designated bank account, customer pays IRAS | Funds are paid directly to IRAS on your behalf | ||

| Fee | 0.5-3% | 1.99% (until 30 June, with promo code MILELIONTAX, Visa or Mastercard) | 1.99% (until 31 July, with promo code TAX199, Visa only) | 2% |

| Cost Per Mile | Theoretical: 1.14 Realistic: 2.10 |

Theoretical: 1.22 Realistic: 1.30 |

Theoretical: 1.22 Realistic: 1.30 |

Theoretical: 1.25 Realistic:1.67 |

| Limit | Amount stated on Notice of Assessment | |||

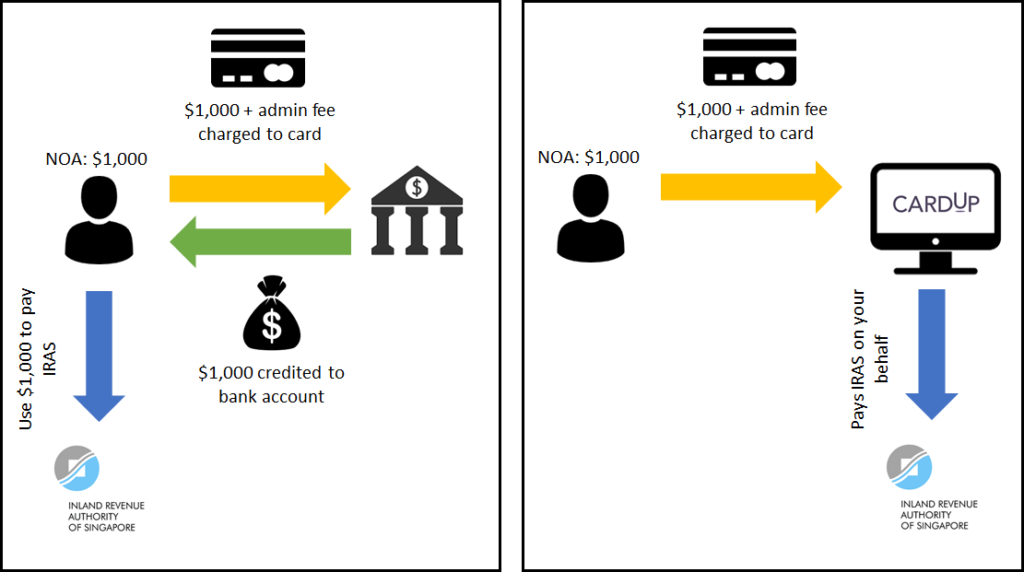

Bank vs Third Party: The Difference in Payment Mechanisms

Bank payment facilities work very differently from third party ones.

With the former, you submit your NOA and designate a bank account to receive funds. The bank charges your credit card for the tax due amount plus an admin fee, and deposits cash into your designated bank account. You’ll then use that cash to pay IRAS yourself.

Right: Using a third party facility.

With the latter, you submit your NOA to CardUp/ipaymy/PayAll, which charges your credit card for the tax due amount plus an admin fee. CardUp/ipaymy/PayAll then pays IRAS on your behalf.

In both cases, your net out-of-pocket expenditure is the admin fee, for which you’ll earn miles on your credit card.

Online Payment Platform Admin Fees: Are They Worth Paying?

Regardless of whether you choose a bank or third party payment facility, you’ll have to pay an admin fee to earn your miles.

That said, it’s a mistake to look at the fee in isolation.

For example, HSBC advertises an admin fee of 0.5% when you pay taxes with your HSBC Premier Mastercard. That’s lower than Standard Chartered’s 1.6% admin fee, so you may think it’s ~3X cheaper.

However, the HSBC Premier Mastercard only earns 0.4 miles per dollar (mpd), while the SCB Visa Infinite earns 1.4 mpd (assuming you spend at least $2K in a statement period).

On a cents per mile basis, you’d pay 1.25 cents with HSBC, versus 1.14 with SCB. The right figure to compare therefore, is the cost per mile, which you derive by taking admin fee divided by mpd.

If you hate doing math, here’s a handy reference table:

Tax Payment Method |

Processing Fee |

Earn Rate |

Cost Per Mile (Cents) |

| Standard Chartered Visa Infinite (≥$2K spend p.m) | 1.6% | 1.4 | 1.14 |

| HSBC Visa Infinite (≥$50K spend in prev year) | 1.5% | 1.25 | 1.20 |

| CardUp with DBS Insignia/Citi Ultima/UOB Reserve | 1.99% till 30 Jun | 1.6 | 1.22 |

| HSBC Premier Mastercard | 0.5% | 0.4 | 1.25 |

| Citi PayAll with Citi Ultima | 2% | 1.6 | 1.25 |

| CardUp with BOC Elite Miles World Mastercard | 1.99% till 30 Jun | 1.5 | 1.30 |

| CardUp with UOB PRVI Miles | 1.99% till 30 Jun | 1.4 | 1.39 |

| HSBC Visa Infinite (<$50K spend in prev year) | 1.5% | 1.0 | 1.50 |

| CardUp with Citi Prestige | 1.99% till 30 Jun | 1.3 | 1.50 |

| Citi PayAll with Citi Prestige/PremierMiles AMEX | 2% | 1.3 | 1.54 |

| Standard Chartered Visa Infinite (<$2K spend p.m) | 1.6% | 1.0 | 1.60 |

| CardUp with DBS Altitude/Citi PremierMiles Visa/OCBC VOYAGE | 1.99% till 30 Jun | 1.2 | 1.63 |

| Citi PayAll with Citi PremierMiles Visa | 2% | 1.2 | 1.67 |

| UOB Visa Infinite Payment Facility (Reserve + Metal) | 1.7% until 31 July | 1.0 | 1.70 |

| HSBC Revolution | 0.7% | 0.4 | 1.75 |

| DBS Insignia | 3.0% | 1.6 | 1.88 |

| OCBC Voyage | 1.9% | 1.0 | 1.90 |

| UOB PRVI Pay | 2.1% | 1.0 | 2.10 |

Consider the Cost Per Mile Based on The Credit Card You're Using

You’ll notice I’ve mentioned a theoretical and realistic cost per mile figure in the table up top.

Theoretical refers to the lowest possible cost. For example, you can use the HSBC Visa Infinite to pay your taxes at a cost of 1.2 cents per mile, but to qualify for the card in the first place, you need an annual income of at least $120,000. Similarly, you can use the DBS Insignia and CardUp to pay your taxes at a cost of 1.22 cents per mile, but you need an annual income of at least $500,000 to qualify.

I’m guessing most of us will be some distance away from that, which is why I’ve provided the “realistic” figure for an alternative perspective. This is calculated based on credit cards which are available to anyone at the $30,000 income level.

For example, holders of the UOB PRVI Miles card can use the PRVI Pay facility to pay income taxes and buy miles at 2.1 cents each. Likewise, holders of the Citi PremierMiles Visa card can use PayAll to pay income taxes and buy miles at 1.67 cents each.

There is a Limit to How Many Miles You Can Earn with Income Tax

If your NOA states your tax bill is $5,000, you can’t ask the bank to transfer $10,000 into your account. Similarly, you can’t ask CardUp/ipaymy/PayAll to pay $10,000 on your behalf, even if you’re willing to pay for the additional miles. This effectively sets a cap on the number of miles you can buy when paying your income taxes.

However, because banks don’t pay IRAS on your behalf, there’s nothing stopping you from using multiple bank payment facilities, assuming you have the right cards. For example, I could apply for both the HSBC and Standard Chartered tax payment facilities, thereby doubling the number of miles I buy.

Where third party facilities are concerned, you could use CardUp and ipaymy and PayAll at the same time, but the end result is that your tax bill will be overpaid and it will take some time to receive a refund.

Conclusion

Here’s the crux of the matter: whether or not the fee is worth paying depends on how do you value a mile?

The gold standard for buying miles is to pay no more than 2 cents each (although some would argue that with the recent KrisFlyer devaluation, the value should be closer to 1.7/1.8 cents), so generally speaking, any option that yields miles below this price is worth considering.

That said, if you have no trips planned in the near future, it’s not a good idea to buy miles speculatively. Miles aren’t a good investment to hold, because they don’t earn interest, they don’t have deposit insurance and their value can only decrease over time.

How far is the near future? That depends on the price you’re paying per mile. If you buy miles at the lowest end of the spectrum (for example, at 1.14 cents each) with the SCB Visa Infinite card, you can afford to hold on to them longer than someone who buys miles through UOB PRVI Pay at 2.1 cents each.

That’s how you pay taxes with your credit card. Be sure to do the math and find out if it works for you!

Read these next:

How to Earn Rewards and Miles for Paying Your Income Tax

Singapore Start-Up Disrupting How You Pay Rent, Taxes and Insurance Premiums

How to Earn Miles on Bus and MRT Rides

‘I Have 19 Credit Cards But There’s Just Three You Need to Have’

Do You Have a Passive Income Strategy?

Similar articles

6 Ways to Turbocharge Your Travel Hacking Game

4 Questions To Ask Before Requesting For A Credit Card Annual Fee Waiver

SC EasyBill Vs Citi PayAll: Which Is Better?

How Can You Earn Miles When Paying Tuition Fees?

Best Bill & Tax Payment Services That Still Earn You Rewards & Miles In Singapore

How To Pay Income Tax With Credit Cards For Miles & Rewards

Singapore Startup Disrupting How You Pay Rent, Taxes and Insurance Premiums

Column: How Do People Stay Rich When Their Business Goes Bankrupt?

Back to Blog

Back to Blog