Opportunities to reduce your income tax in Singapore are aplenty. You can also have your cake and eat it too, by investing the money that you save. Here’s how to go about it.

A 1716 play written by British playwright Christopher Bullock, dubbed The Cobbler of Preston, contains a line that has endured more than three centuries later: “Tis impossible to be sure of anything but Death and Taxes”.

It’s a tad morbid but at least folks working in modern-day Singapore have a bevy of income tax reliefs that ease the burden of the latter surety.

To sweeten the deal, several income tax reliefs are ‘built-in’ and don’t require you to make any claims. For example, NSmen are entitled to an income tax relief ranging from S$1,500 to S$5,000 per year, depending on what conditions are fulfilled.

If you’re an NSman’s spouse, you automatically receive a S$750 income tax relief every year too.

That’s not all, because you can double dip and direct the money saved on taxes to your investments. “Wealth begets wealth”, as they say. To get you started, here’s a full guide to optimising your annual income tax.

Also, discover how this leads to better investment returns and which is the best platform out there that you can utilise.

Table of contents

- What income tax reliefs are available for me?

- How much do I really get to save every year?

- How does this lead to better investment returns?

- Which is the best investment platform that I can utilise?

- Conclusion

What income tax reliefs are available for me?

In a word: plenty. Singapore’s business-friendly environment means that there are a plethora of opportunities for taxpayers to optimise their income tax.

IRAS states that these tax deductions are doled out to ‘encourage social and economic objectives such as filial piety, family formation and the advancement of skills’.

The table below highlights several income tax reliefs which fulfill these objectives.

| Income Tax Relief | Amount | Qualification Requirements |

| Course Fees Relief | Up to S$5,500 annually | - Attend a course/seminar/conference that awards an approved qualification - Approved qualification can be academic, professional, or vocational - No limit on the number of courses that can go towards claims for this relief |

| Earned Income Relief | Up to S$8,000 annually, up to S$12,000 for handicapped persons | - S$1,000 for those below 55, S$6,000 for those 55 to 59, S$8,000 to 60 and above - For handicapped persons: S$4,000 if you're below 55, S$10,000 if you're 55 to 59, and S$12,000 if you're 60 and above - You'll be eligible for the relief if you have taxable income from these sources in the previous year: employment; pension; or trade, business, profession or vocation |

| Parenthood Tax Rebate | As outlined | - S$5,000 for the first child, S$10,000 for the second child, and $20,000 for ther third and subsequent child. The child must be a Singapore Citizen at the time of birth or within 12 months thereafter. |

| Qualifying Child Relief (QCR)/Handicapped Child Relief (HCR) | S$4,000 per child (QCR)/ S$7,500 per child (HCR) annually | - Child must be at least 16 years old or studying full-time - Child must not have drawn an annual income of at least S$4,000 |

| Grandparent Caregiver Relief | S$3,000 annually | - Claimant must be a working mother who’s married, divorced, or widowed - Unemployed parents or grandparents lived in Singapore for at least 8 months and took care of any of your children - Child must be Singaporean below 12 years old or unmarried and handicapped |

| Working Mother’s Child Relief | 15% of earned income for the 1st child. From 1 January 2024, the relief will be a fixed amount of up to S$12,000 | - As announced in Budget 2023, from 1 January 2024, the relief will be a fixed amount: S$8,000 for the first child, S$10,000 for the second child, and S$12,000 for the third child and beyond - Child must be a qualifying Singaporean born or adopted on or after 1 Jan 2024. |

Then there’s the Supplementary Retirement Scheme (SRS), which was introduced in 2001 by the Ministry of Finance. In essence, every dollar that’s deposited in your SRS account is matched with an equal amount in income tax relief.

Annually, this is capped at S$15,300 for Singaporeans and Permanent Residents and S$35,700 for Foreigners.

These schemes mentioned are just the tip of the income tax relief iceberg, with many more that working professionals in the Lion City can take advantage of.

Take cash donations to the Community Chest or approved Institutions of a Public Character, for example. Individuals who make a qualifying donation are granted a 250% income tax deduction based on that amount. Furthermore, donations aren’t subject to any income tax relief limits.

While there are indeed many opportunities available for individuals in Singapore to optimise their income tax, do note that deductions have an annual limit of S$80,000.

As mentioned above, donations do not contribute to this limit, so it’ll be the only way to avoid the taxman when your annual income hits S$100,050.

Also read: CPF Contribution Ceiling Increase – How Does it Affect You?

How much do I really get to save every year?

It’s one thing to state the various income tax reliefs that are available, but another to put these deductions into practice. Several are automatically applied, but keep in mind the reliefs that require you to put in some legwork.

Find out how much you realistically stand to save annually from income tax deductions through these personas detailed below.

Jack: Singaporean, 30 years old, single, NSman, S$80,000 annual income (not including employer’s CPF contributions)

From the outset, Jack is subject to an income tax of S$3,350. However, this drops by more than 30% to S$2,342 once his CPF Relief kicks in. Throw in the Earned Income Relief of S$1,000 and it’s now S$2,272.

And assuming Jack was called up for reservist duties the previous year, the NSman Self Relief pushes this figure down to S$2,062.

Lastly, if he deposits 15% of his annual income into his SRS account, the final income tax he’ll need to pay is just S$1,222. It might not stop the taxman from knocking on his door completely, but S$1,222 is much lower than S$3,350.

Total amount saved: S$2,128 (2.6% of annual income)

Jill: Singaporean, 40 years old, married, mother of one, S$120,000 annual income (not including employer’s CPF contributions)

As Jill draws a higher salary, her income tax would be S$7,950 without tax reliefs. Like Jack, this figure drops significantly post-CPF Relief to S$6,294.

The Earned Income Relief then reduces this to S$6,179. Furthermore, Jill is entitled to the S$4,000 Qualifying Child Relief. Her income tax now stands at S$5,719.

That’s not all, because Jill benefits from the Working Mother’s Child Relief (assuming that her child was born before 2024). This lowers her taxable income tax to S$112,000 just S$3,649. Factor in the NSman Wife Relief and it’s now S$3,562.75.

Jill can make a S$5,500 claim under the Parent Relief for supporting her retired parents as well, bringing her income tax to S$3,094.50.

Finally, if she deposits 10% of her annual income into her SRS account, her final income tax clocks in at S$2,254.50. The taxman won’t stop visiting her, but the amount payable is much more manageable now.

Total amount saved: S$5,696 (4.7% of annual income)

How does this lead to better investment returns?

As mentioned, the money that you save through optimising your income tax can be used to accelerate your wealth accumulation plans. An extra S$2,000 to S$7,000 per year is nothing to scoff at, as every dollar saved is a dollar earned.

If you invest your SRS monies in the equities market prudently over a longer period of time, i.e. 20 to 30 years, you can expect returns around 7% to 9% p.a. Given that the SRS account only earns 0.05% p.a., investing your SRS funds beats inflation and helps to ensure that you’ll retire comfortably.

Here’s a comparison between investing your SRS funds and leaving them in the account across five years. The annual deposit used in this example will be S$15,300, which is the maximum amount eligible for income tax deductions for Singaporeans.

Projected returns on your invested SRS funds is computed in the table below at 9% p.a.*

SRS account value, with S$15,300 annual top-ups

| Year | SRS contributed | SRS (invested) | SRS (uninvested) |

| 1 | S$15,300 | S$15,300 | S$15,300 |

| 2 | S$30,600 | S$31,977 | S$30,607.65 |

| 3 | S$45,900 | S$50,154.93 | S$45,922.80 |

| 4 | S$61,200 | S$69,968.87 | S$61,245.77 |

| 5 | S$76,500 | S$91,566.07 | S$76,576.39 |

Although investment returns aren’t guaranteed, the potential upside after five years is S$14,989.68. That’ll go towards several well-deserved vacations to celebrate your retirement or even close to a year’s worth of expenses.

And with more investment options being added as the years go by, there’s no better time to start making the most out of your SRS funds.

Which is the best SRS investment platform that I can utilise?

The Ministry of Finance has stated that there’s no limit to what you can invest your SRS funds in, as long as the provider supports deposits from your SRS account. It’s much less restrictive than the CPF Investment Scheme, but individuals are subject to choice overload.

There are some considerations around investing SRS monies:

- You have a long investment horizon, and hence would be able to take more risk with SRS investments

- You are not able to invest in overseas stock exchanges due to SRS restrictions

- As you are not able to withdraw dividends earned until retirement, it is better to invest for long term capital gains

How do you decide which is the best SRS investment platform to go with?

When you’re growing your retirement funds, you’d want a platform that’s low-cost and grants access to a diversified portfolio. This allows you to reduce your investment risk and gives you the best chance of success for your retirement nest egg.

Enter robo-advisor Endowus. Not only does it allow you to invest with your SRS funds, you can make cash investments and utilise your CPF funds too.

Founded in 2017 and offering investment portfolios to retail investors by 2019, Endowus’ motto is to provide low-cost access for its users. This allows investors to grow their wealth at a quicker pace as they get to keep more of their returns.

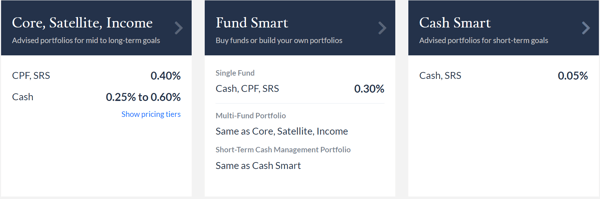

Here’s a complete look at Endowus’ fee structure across its portfolios when investing using your SRS funds.

Yes, Endowus’ fees are indeed that straightforward when you’re investing with your SRS funds. There’s no catch either. You aren’t subject to any lock-in periods and there’s no need to worry about miscellaneous charges such as deposit and withdrawal fees.

Simply select the portfolio that you’d like to invest in, make a lump-sum or recurring deposit, and let Endowus do the rest.

The funds that Endowus invests in are from the world’s top fund managers as well. These include BlackRock, Dimensional Fund Advisors, PIMCO, and more. Rest assured that you’re getting access to top quality investment funds at a low cost.

Conclusion

Tax season is never a pleasant time, no matter which country you’re living in. Fortunately, the multitude of income tax reliefs in Singapore makes the pinch hurt a lot less. What’s more, you’re given the opportunity to double dip by using the money saved to grow your wealth. Who says you can’t have your cake and eat it too?

The SRS provides yet another avenue for you to double dip, with income tax deductions being granted for deposits into your SRS account.

From there, you can use the funds to invest in a low-cost and diversified portfolio through a roboadvisor or online brokerage. It’s a sensible decision to make, no matter whether you’re a beginner investor or seasoned stock-picker.

No one in their right mind enjoys paying taxes, but you know what they say about making lemonade out of lemons. And you’ll have plenty of lemonade to go around when you optimise your income tax and invest intelligently thereafter.

This article was written in partnership with Endowus.

Disclaimers: Investment involves risk. Past performance is not necessarily a guide to future performance or returns. The value of investments and the income from them can go down as well as up, and you may not get the full amount you invested.

Rates of exchange may cause the value of investments to go up or down. Individual stock performance does not represent the return of a fund.

Any forward-looking statements (including projections) contained in the information on this article, including in any document or communication posted on this website, are estimates only. Such projections are subject to market influences and contingent upon matters outside the control of Endowus and therefore may not be realised in the future.

Please note that the above information does not purport to be all-inclusive or to contain all the information that you may need in order to make an informed decision. The information contained herein is not intended, and should not be construed, as legal, tax, regulatory, accounting or financial advice.

Please note that the above information does not purport to be all-inclusive or to contain all the information that you may need in order to make an informed decision. The information contained herein is not intended, and should not be construed, as legal, tax, regulatory, accounting or financial advice.

You should carefully consider whether any investment views and products/ services are appropriate in view of your investment experience, objectives, financial resources and relevant circumstances or seek financial advice from Endowus’ platform.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

Read these next:

Best Annuity Plans For Your Retirement In Singapore

Comparing The Returns & Fees Of The Top Robo-Advisors In Singapore (2021)

Beginner’s Guide To CPF Retirement Sums And How To Get There (2021)

Guide To Supplementary Retirement Scheme (SRS) And Tips To Maximise It

A Guide To Leaving A Legacy In Singapore

Similar articles

All You Need To Know About Income Tax In Singapore

3 Reasons Why You Should Start Investing With A SRS Account

Guide To Supplementary Retirement Scheme (SRS) And Tips To Maximise It

Have a More Comfortable Retirement Through Tax Optimisation: SRS

What To Know About Income Tax Relief Season

How Can I Maximise My Investment Returns with S$1k?

In the Millionaires’ Club? Here's how to Optimise Your Tax Efficiency

How Much Taxes to Pay in Singapore (If You’re an Expat)?

Back to Blog

Back to Blog