The world over, every parent dreams of giving their child a good education.

There is no doubt in parents’ minds that this is the key to ensuring a bright future for their children. So, many of them start thinking quite early on about ways to save money for their children’s future

Parents in Singapore are no different.

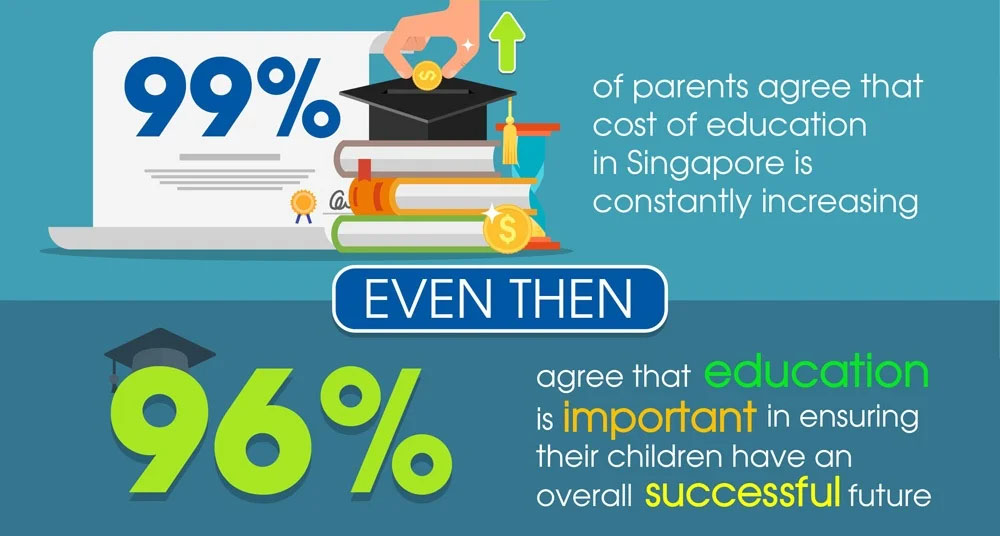

theAsianparent conducted a survey commissioned by dollarDEX in Singapore and found that 96% of parents here are convinced of the importance of education to secure their kids’ future.

The rising cost of education

In today’s world of financial volatility and uncertainties, the cost of education is rising, like all major services worldwide. In Singapore, a report by CNBC suggests that the cost of attending university has jumped 38% on average since 2007. The annual tuition fees for a general arts and science degree used to cost between S$6,000 to S$7,000 back in 2007. However, the same degree costs between S$8,000 and S$11,000 today, which is up as much as 51%. Similarly, at the Singapore Management University (SMU), the same degree cost S$7,500 in 2007, which was also the most expensive among the other local universities. Today, it is going to set you back by S$11,300 in SMU at a whopping 50% jump in fees.

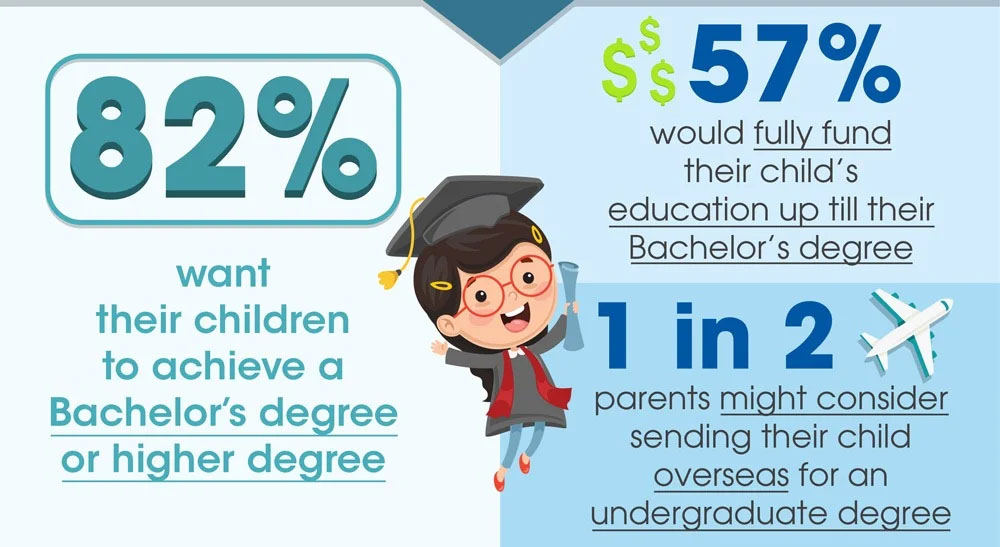

Despite these soaring costs, parents still want the best for their children, and most would prefer a bachelor’s degree or even higher for their children.

Of course, for your child to acquire at least a bachelor’s degree, the cost has to be borne either by you or your child, likely through a student loan or scholarship. While student loans may be common in western countries, most Asian parents shoulder this cost for their children.

Besides paying for tuition fees and living expenses for their children, some parents are also keen to explore overseas education in the US, the UK or Austraila where the quality is deemed to be higher.

Funding for your child’s university education is definitely not cheap, let alone sending them overseas for it. So, how is it possible to ensure you have sufficient funds to do so?

How much will you spend on your child’s education and what is a smart way to accumulate funds for it?

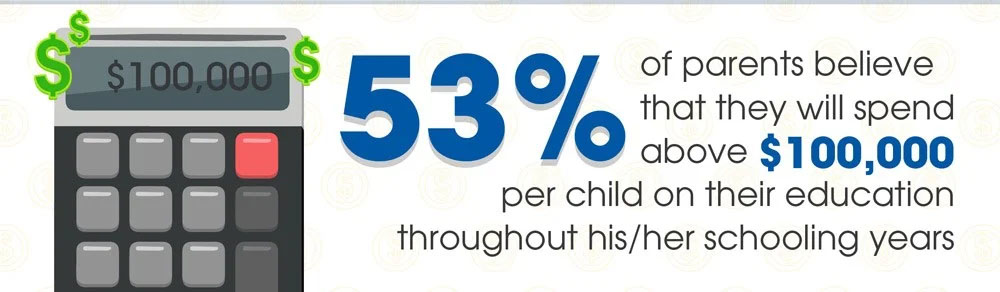

We all love our children and want to support in what they do, including their education. But when we do the math, the investment required is staggeringly high.

Here is an estimated breakdown of investment in education you will be making for your child in Singapore throughout their schooling years:

- Primary and Secondary School education: approximately S$2,136 for 14 years of studies in Government schools

- Junior College: approximately S$792 for two years of studies

OR

- Polytechnic: approximately S$8,700 for three years of studies

- University degree: approximately S$28,000 to S$146,750 (depends on the course of study)

For example, the tuition fee for NUS approximately ranges between S$29,650 – S$146,750, depending on the course.

If you project this 10-15 years from now, the costs will likely be even higher. Have you ever given it a thought and done the calculations? Here’s what other parents think.

Have you started saving for your child’s education?

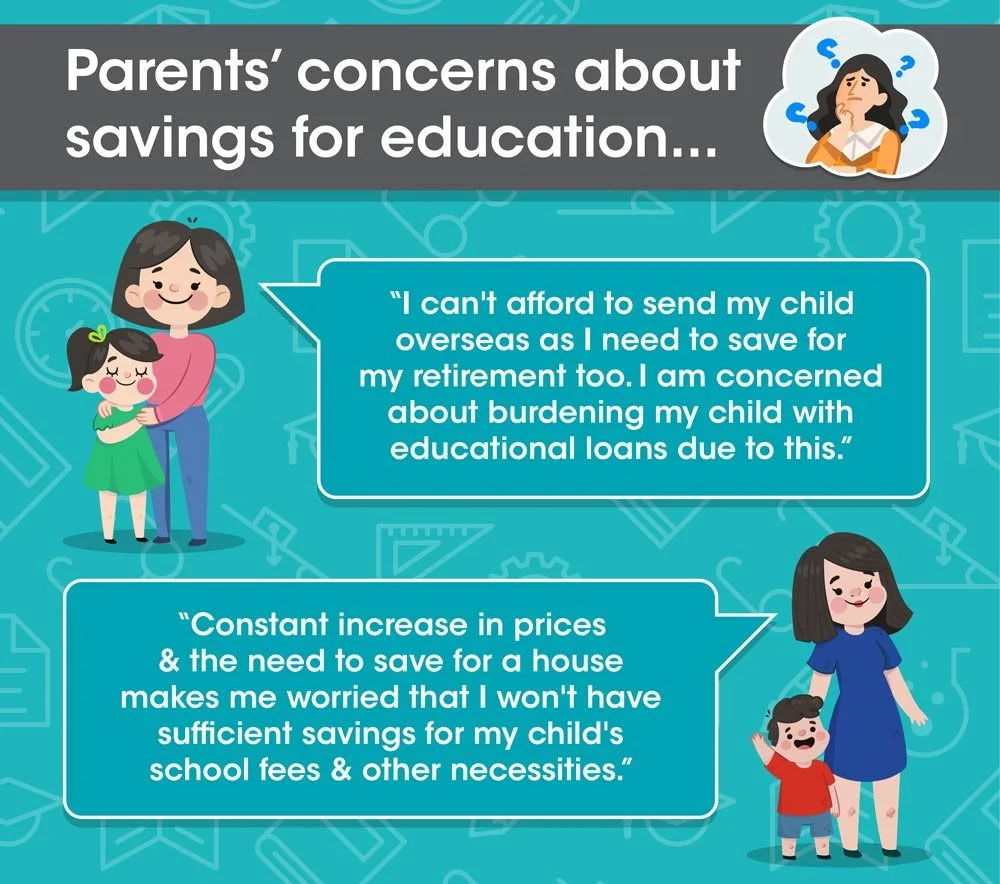

Paying for your child’s university education is probably one of your biggest financial concerns. There might be other competing demands on your income that disrupt your saving plans such as home mortgage, car loans, school and tuition fees, healthcare and travel costs.

Top 3 reasons why parents haven’t started saving for their child’s university education

Sometimes, parents have all the good intentions to save money for their child’s future education. However, they tend to delay saving for one reason or another. Here’s what we found out in our survey (please see the right side of the infographic below, titled 'Top 3').

Top 3 ways to fund your child’s university education

So are you a procrastinator when it comes to saving for your child’s college education?

It’s time to be proactive! After all, it’s about your child’s future. You can plan to start saving as early as you can afford to. This can help reduce the burden on you in the future or your child so they won’t have to take up a student loan, which helps them remain debt-free.

To put this in perspective, one research has found that more than 52% of parents in Singapore are willing to go into debt to fund their child’s university education and is probably the biggest financial hit you will take, besides your property. This makes it even more important for you to start planning for your child’s education much earlier.

While there are various financial instruments that can help you in this regard, choosing one is not easy, especially if you are not financially savvy.

Which product should you choose to save money for your child’s education? Should you just put your money in an ordinary savings account or should you go for a portfolio of stocks and bonds? What about an insurance policy that matures in the future? There are many options out there.

What’s more, they can be confusing with differing entry amounts, liquidity and maturity dates. It can all potentially lead to analysis-paralysis in parents.

Here’s the top 3 products that most parents are planning to use to save for their child’s university:

Different savings approaches at different stages of life

The act of saving for the future is dependent on what life stage you are in. If you are a young parent, you might think that you have plenty of time ahead to save for your child. Maybe your priority right now is to invest in a house.

Slightly older parents might be worried about saving for their retirement.

But it’s never too late…

The best approach for parents when saving money for their child’s education, is to have multiple engagements within the financial eco-system. This gives you a mix of different financial products with different maturity or liquidity to manage your future finances.

In other words, don’t put all your eggs in one basket by having a mix of insurance policies, cash in savings account, investments and even fixed deposits, depending on your needs.

If you haven’t started saving for your little one’s future education, it is never too late to start now. You just have to find the right plan that works for you.

There are options to sign up on online investment platforms such as dollarDEX (backed by Singlife) to ensure a worry-free plan that can help you save for your child’s future education.

Some of the benefits of a platform such as this include:

- Liquidity: You can withdraw the money whenever you need it.

- Low investment sum: A Regular Savings Plan that is flexible for everyone including parents with commitments. You can invest starting from just $100/month, and increase along the way when you can afford to, or when you get a pay increment!

- 24-hour monitoring: You can log in 24/7 and carry out/monitor your investments at any time even when you are commuting home or after putting the children to bed.

- Low fees: Invest at a low rate or incur no fees. For example, the low fee of around $100 per month goes straight into the fund of your choice.

Investing in your child’s future education need not be complicated or require a lot of money. What's most important is that you start planning for the best possible higher education for your child at the right time.

A version of this article was first published on The Asian Parent.

Read these next:

Retirement Planning: It’s For Your Kids Too

Parental Monthly Allowance: How Much Is Enough and Fair?

How to Save Money on Maternity Costs in Singapore

‘Why I’m Not Saving Up For My Kids’ University Fund’

Joanne Peh Shares Travel Tips After Family Holiday Nightmare

Teaching Kids About Money: 5 Fun Ways

By The Asian Parent

theAsianparent is the largest parenting website in Southeast Asia. Got a parenting concern? Read articles or ask away and get instant answers on our app. Download theAsianparent Community on iOS or Android, now!

Similar articles

An 8-Step Plan to Saving S$80,000 for University in Singapore

‘Why I’m Not Saving Up For My Kids’ University Fund’

Parents: Here’s Why You Shouldn’t Dip Into Your Child’s Savings

How to Find the Best Education Endowment Plan in Singapore

Parental Monthly Allowance: How Much Is Enough and Fair?

How to Save for Your Child’s University Education

Retirement Planning: It’s For Your Kids Too

Holiday With Ease With These 5 Brilliant Travel Products For Kids

Back to Blog

Back to Blog