You often hear people say that you should ‘buy the dip’ when the market is down. But just what does buying the dip mean, and should you include it into your investment strategy?

‘Buy the dip’ is a popular term among investors, and you may have heard of it at some point in your investment journey.

In essence, buying the dip is akin to the ‘buy low, sell high’ principle whereby you buy a stock that’s fallen in price, with the expectation that it will rebound in the future.

In this article, we’re going to explain how the buy the dip strategy works, the caveats of buying the dip and how to manage the risk associated with this strategy.

What does buy the dip mean?

Simply put, when you ‘buy the dip’, you’re basically buying an asset, such as a stock, after it ‘dips’ in price. Usually, this happens when there’s a sharp decline in the stock price due to broad market fears, such as a pandemic or war.

However, it could also be down to the company’s performance, growth prospects, and poor forecasts, among other things. Therefore, before deciding to buy the dip, it’s crucial to dig deeper into the underlying reasons for the price drops.

Some investors see buying the dip as an opportunity to buy a stock at a ‘discount’ price and make a profit when the price rebounds (or better yet, eclipses its previous high). This helps to bring down the average price of buying the stock, also known as averaging down.

Basically, averaging down means that you buy additional shares of the stock after it falls in price. By buying an asset at a lower price, you’ll don’t have to wait for prices to rise too high to start making a profit. For example, if you own a stock that’s valued at S$50 per share, you might buy more shares once the price falls to S$40 per share.

Averaging down can be a good strategy if you believe that the stock is just experiencing a short hiccup and is expecting it to turn around.

However, buying the dip usually involves timing the market and comes with huge risks. It also doesn’t necessarily mean that you’ll make money (in fact, you could be losing).

How the buy the dip strategy works

If you’re familiar with the dollar-cost-averaging (DCA) strategy of investing at regular intervals, think of buying the dip strategy the opposite of that.

Instead of using cash to make recurring investments, say for every month, you accumulate your cash and wait for the stock to dip to a certain level. Once that happens, you invest the cash that you’ve stockpiled to buy the dip.

However, determining the specific price ‘dip’ to buy can be tricky, as there’s usually no fixed value for the dip. Some investors choose to buy small dips, while others will take a more strategic approach by setting a benchmark based on the market’s highest level (20%, 30%, 40%, etc.). Once the market falls to that benchmark (say 30%), they’ll invest their saved-up cash to buy the dip.

The general idea of buying the dip is that you get to buy shares at a lower price, and assuming that you hold on to them and the stock continues on an uptrend over time, improve your future gains.

Start managing and saving money like a pro with SingSaver’s weekly financial roundups! We dole out easy-to-follow money-saving tips, the latest financial trends and the hottest promotions every week, right into your inbox. This is one mailer you don’t want to miss.

Sign up today to receive our exclusive free investing guide for beginners!

Caveats of buying the dip

You’re betting that the stock will bounce back to its all-time high (which may not happen)

Unless you’re certain of the business’s outlook and growth, and that the decline is just a temporary blip, you can’t be sure whether the stock will rebound after the dip. If it doesn’t recover, you would constantly be buying the dip or making huge losses.

If the market keeps going up, the money never gets invested

Say you’re saving up cash and waiting for the market to fall to a certain threshold so that you can invest. However, if the market doesn’t fall to that level, you would be sitting on lots of uninvested cash for years.

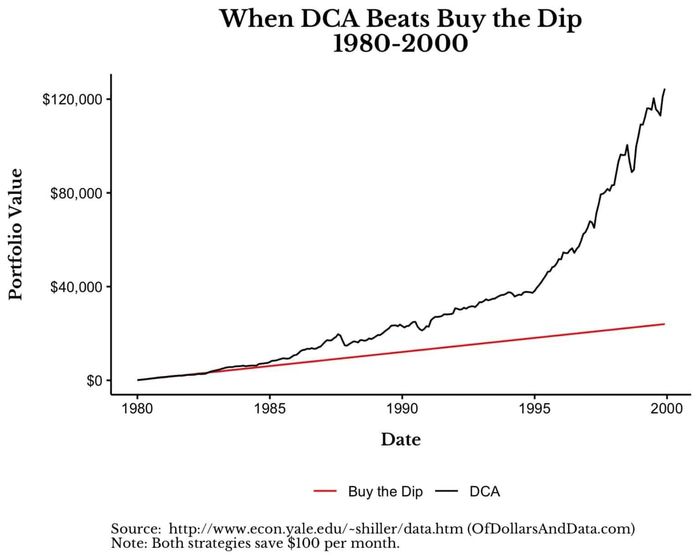

Although an extreme example, the chart above compares buy the dip and DCA. If you had followed the buy the dip strategy by saving US$100 a month and setting a 50% dip benchmark, you would be sitting on lots of uninvested cash for a period of 20 years. That’s because from 1980 to 2000, there were no 50% dips.

In contrast, if you had invested US$100 every month via the DCA strategy, you would be making 5X the gains over the same period as the market soared upwards.

It’s a risky way to invest in the long-term

Buying the dip usually involves timing the market, which is hard to predict. Furthermore, most investors have trouble distinguishing between a short-term blip and warning signs of a long-term downward trend.

As mentioned previously, there are many reasons why a company’s share price might fall; it could be down to core issues within the company such as scandals, or it could also be due to dismal company performance, negative outlook, or economic factors.

How to manage buying the dip

Despite the risks, buying the dip has been successful for many investors and there are ways you can manage the risks and incorporate it into your investment strategy.

Decide when to cut your losses

When you buy the dip, it’s important to manage your risk and set a benchmark so that you can limit your losses. For example, say if a stock falls below your benchmark of S$10, you may want to cut your losses before it continues to fall.

Pick stocks that you think are undervalued

In value investing, you look for a stock that is underpriced and trading below the company’s intrinsic worth. Usually, corrections in the stock are based on the market reacting to negative news and not because of the company’s financial well-being. Conversely, just because a stock becomes cheaper due to a dip doesn’t immediately make it an asset to your portfolio.

However, this isn’t a walk in the park as it requires a lot of homework, including looking at investment metrics such as price-to-earnings ratio, price/earnings-to-growth ratio, and dividend yields. It takes time, but learning the difference between an undervalued stock vs one that may go down much lower will pay off in making wiser investing calls.

Set a specific benchmark to buy the dip

If you’ve done your due diligence and decided to buy the dip when a stock falls to 20%, don’t wait till it drops further. Big dips are rare and you might miss the opportunity to buy the stock when it’s cheap.

Ready to invest into the equity market?

Compare the best online brokerages in Singapore and checkout the latest promos available on singsaver.com.sg

Read these next:

Dollar-Cost-Averaging vs Lump Sum Investing In Singapore: Which Should You Choose?

Best ETFs In Singapore For Tracking Stocks, Bonds And REITs

All The Hidden (And Not-So-Hidden Fees) To Know About When Investing In Stocks

Investing In Exchange Traded Funds (ETFs): A Newbie’s Guide To Getting Started

6 Alternative Investments To Diversify Your Portfolio

Similar articles

Why Is Sea Limited Stock Dropping And What Should Investors Do?

Take This Before You Go: A Must-Read Guide For Budding Investors

Elon Musk’s US$44 Billion Twitter Bid: What Does This Mean For Twitter And Should Investors Be Worried?

What Do Investing Terms Like ‘Paper Hands’ And ‘Diamond Hands’ Mean?

Dollar-Cost-Averaging vs Lump Sum Investing In Singapore: Which Should You Choose?

4 Investing Strategies To Navigate Singapore’s Stock Market

Gender Investing Gap – Should Women Invest Differently?

Should You Buy Shares of Kimly’s IPO?

Back to Blog

Back to Blog