Best Unlimited Cashback Credit Cards in Singapore (2025)

Updated: 24 Oct 2025

Written bySingSaver Team

Team

The information on this page is for educational and informational purposes only and should not be considered financial or investment advice. While we review and compare financial products to help you find the best options, we do not provide personalised recommendations or investment advisory services. Always do your own research or consult a licensed financial professional before making any financial decisions.

For bargain hunters and discount lovers, cashback credit cards are a staple in their wallets.

They often have limitations like minimum monthly spend, cashback caps, and category exclusions. These requirements can be quite troublesome, but this is where an unlimited cashback credit card can help.

As its name suggests, unlimited cashback credit cards help to compensate for the above limitations of regular cashback cards. No minimum monthly spend, no cashback caps, and significantly fewer category exclusions — these are just the base advantages of unlimited cashback cards to name a few.

Keep on reading to uncover other benefits of unlimited cashback cards and our personal tried-and-true tactics in using them.

Find the right credit card for you in no time. 💳✨

Compare exclusive offers on SingSaver across cashback, miles, and rewards cards—plus enjoy stackable welcome gifts.

Best Unlimited Cashback Credit Cards

How do unlimited cashback credit cards work?

In a nutshell, unlimited cashback credit cards function similarly to standard cashback credit cards, allowing you to earn a percentage of cash back on your purchases. However, therein lie several key differences:

|

Criteria

|

Unlimited cashback credit cards

|

Standard cashback credit cards

|

|

Cashback

|

Lower earn rates, but unlimited cashback (e.g. 1.5% to 1.7%) |

Higher earn rates, but limited cashback (e.g. 3% to 10%)

|

|

Minimum spend

|

None

|

Ranges between S$600 to S$2,000

|

|

Cashback cap

|

None

|

Depends on card and eligible spend categories

Ranges between S$60 to S$250 per month/quarter

|

|

Spend eligibility (for bonus cashback)

|

Most categories

|

Select categories only

|

Among the two, unlimited cashback cards are undoubtedly more straightforward and fuss-free to use – with no minimum spend requirement, no cashback cap, and no complicated spend categories (although this perk has recently been nerfed for a handful).

However, when it comes to bonus cashback rates, unlimited cashback cards tend to fall short compared to standard cashback cards.

Most unlimited cashback cards only offer 1.5% to 1.7% cashback on most categories, albeit limitless. On the other hand, standard cashback cards provide higher cashback rates of 3% to 10% on specific categories, but with corresponding caps on cashback earned.

As a result, there's no one-size-fits-all solution for cashback cards. The best card choice will depend on your individual spending needs and preferences.

What to look out for when choosing an unlimited cashback credit card?

With that in mind, are there any important factors to consider before selecting and committing to an unlimited cashback credit card?

Well, despite being the easiest to access and most beginner-friendly credit card for first-timers, here are some key points you should be aware of:

Category eligibility still applies (MCCs)

Despite marketing themselves as all-rounded cashback cards that earn cashback on virtually all categories, the keyword here is "virtually". No credit card can be truly free of category exclusivity or exclusions.

In fact, many unlimited cashback cards have recently been weakened in this aspect, with numerous eligible categories now made ineligible by being added to the cards' respective Merchant Category Code (MCC) exclusion lists.

One poignant example is the UOB Absolute Cashback Card (more on that below). It was once heralded as the "king" of unlimited cashback cards, offering the highest cashback rate of 1.7% on the market and allowing cashback on commonly excluded categories like insurance premiums, education fees, healthcare bills, and more. However, these benefits have recently been removed, and these categories are now excluded.

Evaluating your intentions

Everyone has different intentions for opting for a credit card. However, as a baseline, every credit cardholder can be split into three archetypes: cashback lovers, miles chasers, and rewards points hunters.

If you're reading this article, you probably fall into the first category and want to learn more about what unlimited cashback cards have to offer – and more importantly, why you might choose it over a standard cashback card.

Well, one good way to weigh your pros and cons is to consider the purpose of getting a cashback card. Are you seeking to earn bonus rebates in a specific spend category like groceries or ride-hailing services? Or do you have an upcoming big-ticket purchase (like a wedding or home renovations) that'll exceed the cashback cap of standard cashback cards, thus putting the unlimited in unlimited cashback cards to good use? If it's the latter, then the answer is crystal clear.

Annual fees

Another similarity between standard and unlimited cashback cards would be their annual fees. While most credit cards offer a complimentary first-year annual fee waiver, it's still best to check their specific terms & conditions to confirm this. After the first year lapses, these credit cards typically charge a card membership fee – AKA annual fee – which is usually around S$196.20 (including GST).

How to maximise your unlimited cashback earnings?

Frankly, this is almost like a trick question: If you want to maximise cashback, an unlimited cashback credit card isn't the best option since they only net you 1.5% to 1.7% cashback on purchases. In contrast to standard cashback cards, this is obviously an abysmal rate.

Nonetheless, there is still a way to maximise your unlimited cashback earnings. Simply put, you'd want to use these cards for the following expenses:

Big-ticket purchases

While the cost of big-ticket purchases can vary, weddings, home renovation works, home appliances, and electronics generally fall into this category. Oftentimes, these expenses exceed the cashback cap of standard cashback cards, limiting your bonus cashback earning benefit.

Conversely, unlimited cashback cards don't have a cap, so this wouldn't pose any problems. Thus, although you earn a lower cashback rate, you won't have to worry about "missing out" any cashback potential since it remains consistent all throughout.

As a "backup credit card"

Following the same train of thought, an unlimited cashback card is fantastic for supplementing purchases upon exceeding the cashback cap of your standard cashback card.

This is because once the cashback cap is met, the bonus cashback rate of your standard cashback card is reduced to its base rate. For instance, the OCBC FRANK Card requires a minimum monthly spend of S$800 to earn 8% cashback on foreign currency spend, online, and contactless spend. However, this bonus cashback rate is capped at S$100 total cashback per month across all eligible categories. As a result, subsequent spending will only net you 0.3% cashback.

With an unlimited cashback card, you'd continue earning 1.5% to 1.7% cashback instead of just the base 0.3%.

[UPDATE] Best for recurring payments: UOB Absolute Cashback Credit Card

The UOB Absolute Cashback Card offers 1.7% cashback with no minimum spend or cashback. It’s currently one of the highest rebates offered on the market.

Moreover, UOB Absolute Cashback has the least spend exclusions out of all the unlimited cashback cards. Using this card allows you to earn cashback on often-excluded merchant transactions like insurance premiums, school fees, utilities, rent, e-wallet top-ups and more.

[Update!] However, starting 6 May 2024, the 1.7% cashback earned on these oft-excluded merchants will be reduced to the base 0.3% rate – with the exception of MCC 6300 (Insurance Sales, Underwriting, and Premiums) for now, it seems.

Regrettably, it should be noted that the UOB Absolute Cashback Card operates AMEX as its payment processor – which is frequently declined for payments by numerous insurance providers. Thus, you should consult your financial advisor regarding accepted payment methods before proceeding.

Best for AMEX privileges: AMEX True Cashback Credit Card

The AMEX True Cashback Card offers 1.5% cashback on all eligible spending, with no minimum spend or cashback cap.

Compared to UOB Absolute Cashback, it’s not totally immune to spend exclusions. Certain non-eligible categories include balance transfers, annual card fees, cash advance loans, etc.

Otherwise, key categories like healthcare, utilities, telco, education fees, insurance, home renovation, online shopping, and groceries are all qualified as eligible spend.

While 1.5% is the base rebate rate, this card offers a generous 3% welcome bonus cashback on the first S$5,000 eligible spend within six months of card approval.

While 3% rebate is still measly compared to regular cashback credit cards, this figure is the highest promotional rate among unlimited cashback cards.

Moreover, the S$5,000 expenditure is graciously spaced out over a period of six months. Those spending a monthly average of S$850 and above are more than capable of achieving this minimum consecutive spend for six months.

Thuis, you stand to earn a maximum of S$150 through this welcome 3% bonus rate.

But that’s not all. The cashback is instantaneous. There’s no waiting time nor minimum amount to redeem your cashback.

Note: The AMEX True Cashback Card no longer earns 1.5% cashback on GrabPay top-ups.

Best for sign-up rewards: Citi Cash Back+ Credit Card

Another crowd favourite, the Citi Cash Back+ is a mid-tier card because of its 1.6% cashback with no minimum spend or cashback cap. Unfortunately, this card has considerably more spend exclusions than the aforementioned ones.

You can redeem your cash instantly on the go via SMS or via the Citi app in rebate values of S$10, S$20, and S$50.

In any case, it’s still a decent cashback card to funnel all your retail spending towards. But if you need some convincing, give our Citi Cash Back+ Card review a read.

Though its card mechanics might pale in comparison to the previous two cards, Citibank often issues out more attractive sign-up rewards than other banks.

SingSaver Citi Credit Card + Banking Bundle Offer

Score S$500 Cash via PayNow in place of exisiting rewards when you apply for a Citi Credit Card, make a minimum spend of S$500 and hold a valid Citi banking account (existing or newly opened) by the end of the month following card approval. Valid till 31 July 2026. T&Cs apply.

SingSaver Exclusive Offer

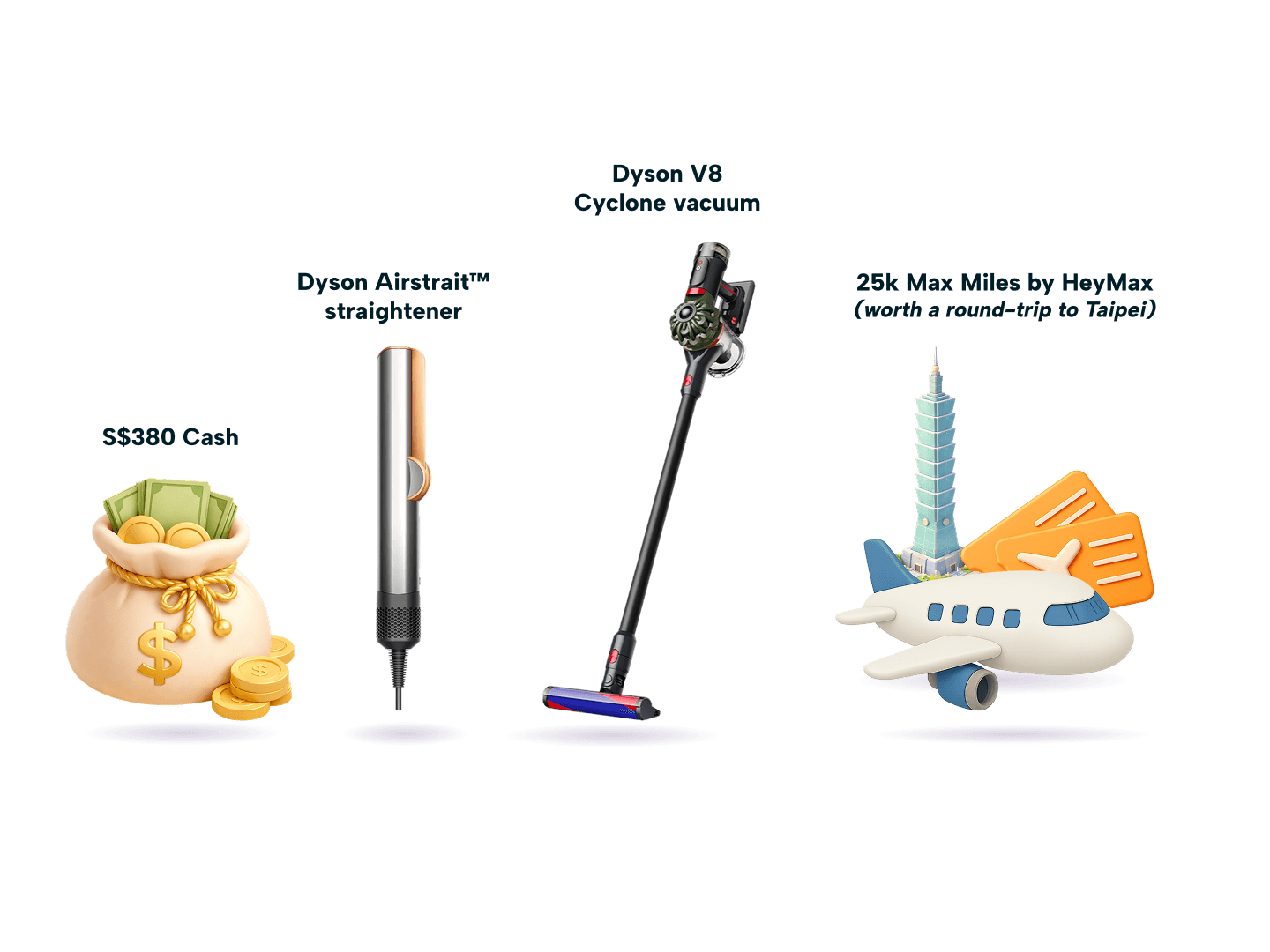

Apply for a Citi Cashback+ Credit Card via SingSaver and score upsized S$420 Cash, 25,000 Max Miles by HeyMax (worth S$600 in travel value), Dyson Airstrait or V8 Cyclone cordless vacuum, or Sony WF-1000XM6 (Earbuds) + S$80 eCap bundle upon activating and spending a minimum of S$500 within 30 days of card approval. Valid till 16 July 2026. T&Cs apply.

Or, Get the Reward Upgrade You Deserve!

You can also top up from just S$100 to upgrade to the latest Dyson and Apple products, including the latest MacBook Neo 256GB Magic Keyboard. Valid till 2 August 2026. T&Cs apply.

Best for extra bill rebates: Standard Chartered Simply Cash Credit Card

The Standard Chartered Unlimited Cashback Card is another respectable card featuring 1.5% cashback with no minimum spend or cashback cap.

One of its perks includes full cashback when you pay your bills through SC EasyBill function. Furthermore, get up to S$288 rebate* when you activate your physical card and spend S$388 on eligible merchants within 30 days of card approval.

If you need further information, maybe our Standard Chartered Unlimited Credit Card review can help.

*Accurate as of time of writing

SingSaver x SCB Simply Cash Card Exclusive Offer

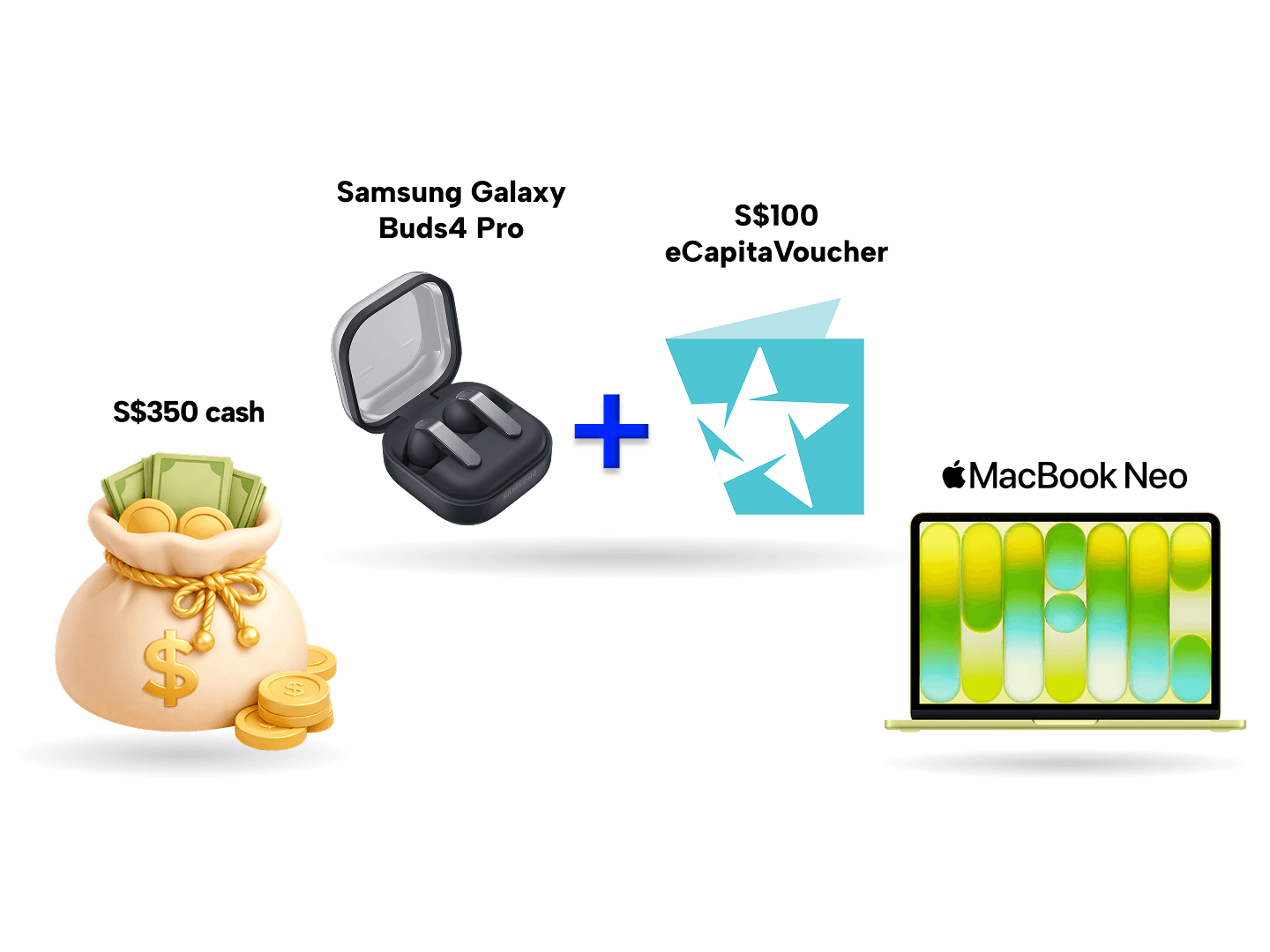

Get a Samsung Galaxy Buds4 Pro + 100 eCap bundle (worth S$449) or up to S$370 when you apply for a Standard Chartered Simply Cash Credit Card via SingSaver, spend a minimum of S$800 within 30 days of card approval, and apply for one of these products: EasyPay, Bonus$aver Account, CashOne, or CCFT. Valid till 2 August 2026. T&Cs apply.

Or, Get the Reward Upgrade You Deserve!

You can also top up from just S$100 to upgrade to the latest Dyson and Apple products, including the latest MacBook Neo 256GB Magic Keyboard. Valid till 2 August 2026. T&Cs apply.

Best for highest conditional cashback: CIMB World Mastercard

Last but not least, we have the CIMB World Mastercard offering 2% cashback with no cashback cap, the highest rate among all the cards so far. However, the drawback is that it’s the highest conditional unlimited rebate.

There is minimum spend involved. This 2% rebate is only awarded upon hitting the minimum S$1,000 spend per month. Otherwise, this rate is reduced to 1% cashback for eligible spend less than S$1,000.

There are also restrictions on category eligibility. Only dining, online food delivery*, movies, digital entertainment, taxi rides, ride-hailing, automobile, and luxury goods are entitled to the highest cashback tier.

Other than that, cardholders are also entitled to 1% cashback on other spend categories with a minimum S$500 spend per month.

Compared to other consistent rebates like UOB Absolute Cashback’s 1.7% cashback on almost all categories, this 2% and 1% conditional cashback by CIMB World Mastercard is not as effective.

Read our full CIMB World Mastercard Review here to have a better idea of what it has to offer.

*Applicable to Deliveroo, Foodpanda, GrabFood, WhyQ, and AirAsia Food merchants only

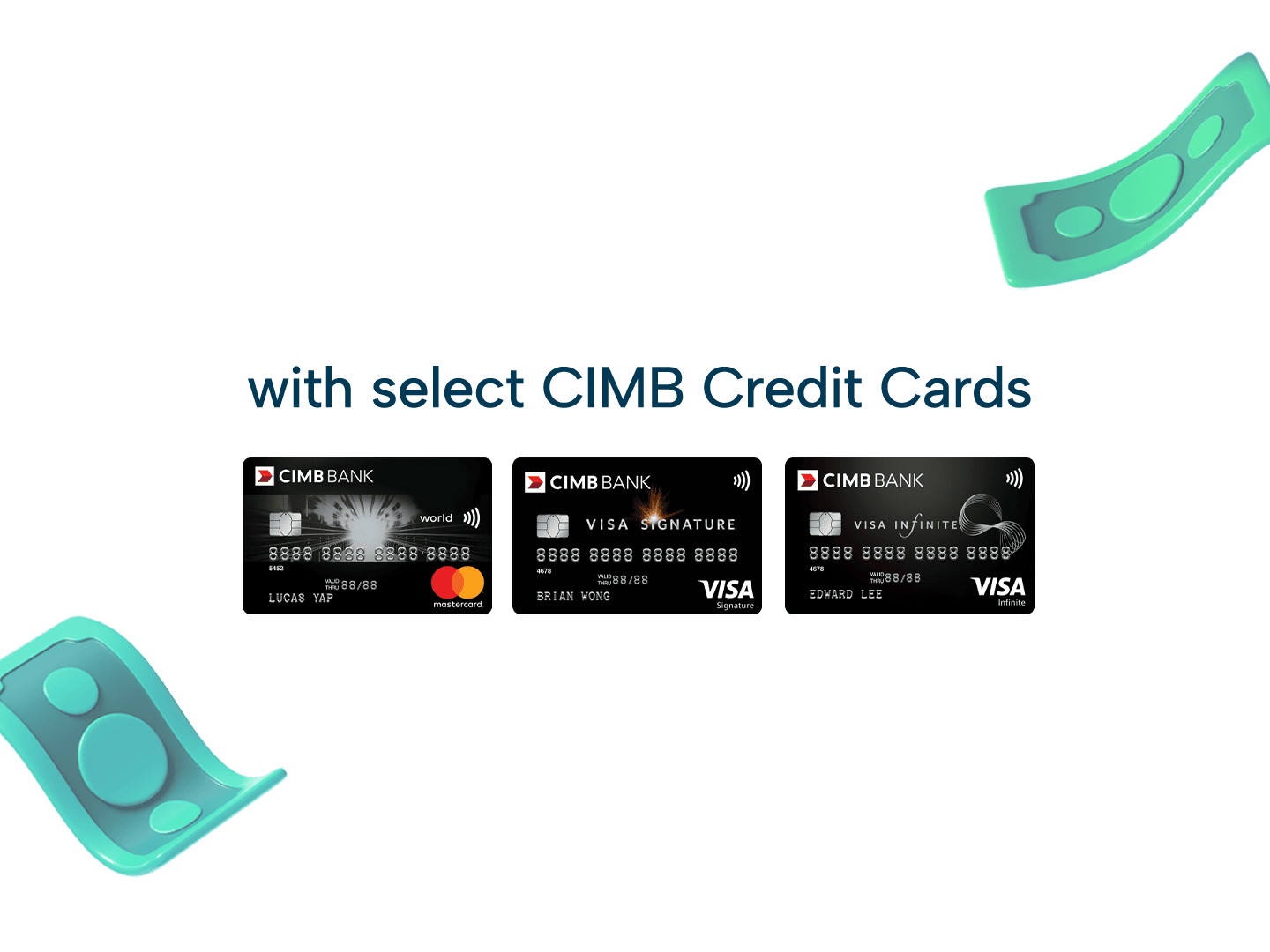

SingSaver x CIMB World Mastercard Exclusive Offer

Receive S$50 Cash when you sign up for a CIMB World Mastercard and spend a min. of S$2,000 within 60 days of card approval. Plus, get an additional Samsonite Black Label Fanthom Spinner 69/25 EXP TSA Luggage (worth S$1,150) fulfilled by CIMB. Valid until 2 August 2026. T&Cs apply.

What other benefits do unlimited cashback credit cards have?

While we’ve covered the basic mechanics of unlimited cashback credit cards, some of you might still be unconvinced of their benefits.

Compared to other cashback cards like UOB One (Up to 15% cashback), OCBC 365 (8% cashback), and POSB Everyday Card (Up to 10% cashback), the <1.7% cashback doesn’t hold a candle to those rebates.

So apart from no minimum monthly spend, no cashback cap, and fewer spend exclusions, why is an unlimited cashback credit card still recommended as a supplement card?

#1: Best for big-ticket purchases & costly household projects

This should be fairly obvious by now but the limitless spending makes these cards ideal for big-ticket purchases and costly household projects. Major purchases like buying your first car can be done through these unlimited cashback cards.

But of course, to be a responsible car owner, you should consider these factors before sealing the deal. After all, not only are cars in Singapore becoming more expensive but they’re more of a luxury than a necessity thanks to our robust public transportation.

Meanwhile, home renovations have also become more expensive. The average home renovation costs around S$30,000 in Singapore, but many couples and families easily exceed this initial budget.

In any case, unlimited cashback cards aren't the only cards capable of footing such costly transactions. Check out these 13 other card recommendations for big-ticket purchases.

#2: Best for bills, fees, and insurance premiums

As stated above, unlimited cashback credit cards like UOB Absolute Cashback and AMEX True Cashback count categories like insurance, hospital bills, utility bills, phone bills, education fees and more as eligible spend.

Hence, it makes sense to consolidate all your important recurring bills into a single card for easier tracking and payment.

#3: Beginner-friendly, especially for young adults

Thirdly, treat unlimited cashback credit cards as your beginner-friendly stepping stone into the world of personal finance.

Too many young adults are over-eager to ‘abandon’ their debit card and apply for their first credit card. This transition symbolises their growth from teenager into adulthood and the newfound freedom that comes with it.

That said, it’s foolish to jump headfirst into a credit card without understanding the responsibilities of managing it. Forgetting to pay credit card bills on time and overspending on credit limits are common mistakes that naive cardholders make.

It’s best to educate yourself on the fundamentals of credit card ownership before committing to one.

Card | Hot Reward Pick | SingSaver Reward | Card benefit | Monthly Spend Required | Annual Fee | ||

|---|---|---|---|---|---|---|---|

| Standard Chartered Simply Cash Credit Card | S$699 | 1.5 % | None | S$196.20 | ||

| Maybank FC Barcelona Visa Signature Card | - | - | 1.6 % | - | S$130.80 | |

| UOB Absolute Cashback Card | S$160 | Up to 1.7 % | None | S$196.20 | ||

| Citi Cash Back+ Card | S$1,499 | 1.6 % | None | S$196.20 | ||

| CIMB World Mastercard | S$1,200 | 1 - 2 % | S$1,000 | No Annual Fee | ||

| American Express True Cashback Card | - | - | 1.5 - 3 % | None | S$174.40 |

Frequently asked questions

Unlimited cashback simply refers to "limitless cashback" that isn't restricted by any cashback caps or minimum spend requirement, unlike traditional cashback credit cards. As long as your purchase qualifies, you'll earn the unlimited cashback rate, typically between 1.5% to 1.7%.

The biggest disadvantage of unlimited cashback cards is their significantly lower cashback rate. Standard cashback cards boast 3% to 10% bonus cashback rates, whereas unlimited cashback cards only provide 1.5% to 1.7%.

Thus, unless you use it for a hefty purchase like big-ticket items, you can't expect a lot of cashback otherwise. You're better off leaving them at home. That's why for everyday spending, standard cashback cards are generally more beneficial.

About the author

SingSaver Team

At SingSaver, we make personal finance accessible with easy to understand personal finance reads, tools and money hacks that simplify all of life’s financial decisions for you.