Opinions expressed reflect the view of the writer (this is his story).

As the year draws to a close and people start to head abroad for holidays, one question on many travelers' minds is "should I use my credit card overseas?" The trepidation is understandable. Using your card overseas may expose you to fraud, incur hefty fees or make you spend more than you'd originally planned.

And yet, banks offer generous miles bonuses for using your cards overseas. You can earn anywhere between 1.6 and 2.5X the miles you'd normally earn on local spending if you use your card overseas.

So does it make sense to use your cards on a holiday? First, however, we need to understand what happens when you use your card overseas.

What fees do you incur on overseas transactions?

When you swipe your card overseas, several things happen.

This means there are three "fees" in play here:

- Implicit foreign currency spread when your transaction is converted to Singapore dollars

- Fee charged by the bank

- Fee charged by the card issuer

(1) tends to be relatively inconsequential, especially if you're dealing with a stable currency like the USD or AUD, so it's really (2) and (3) you want to pay attention to.

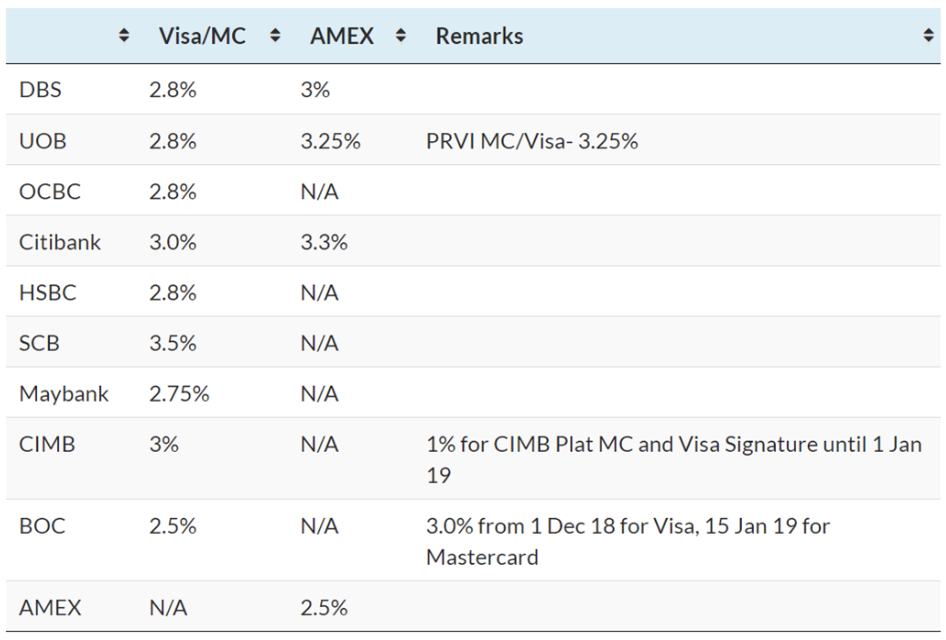

How much does each bank charge?

The table below shows the fees you'll pay for using each of the following bank's cards overseas. For the sake of simplicity, I have combined the bank and card-issuer fees, and ignored the currency conversion spread.

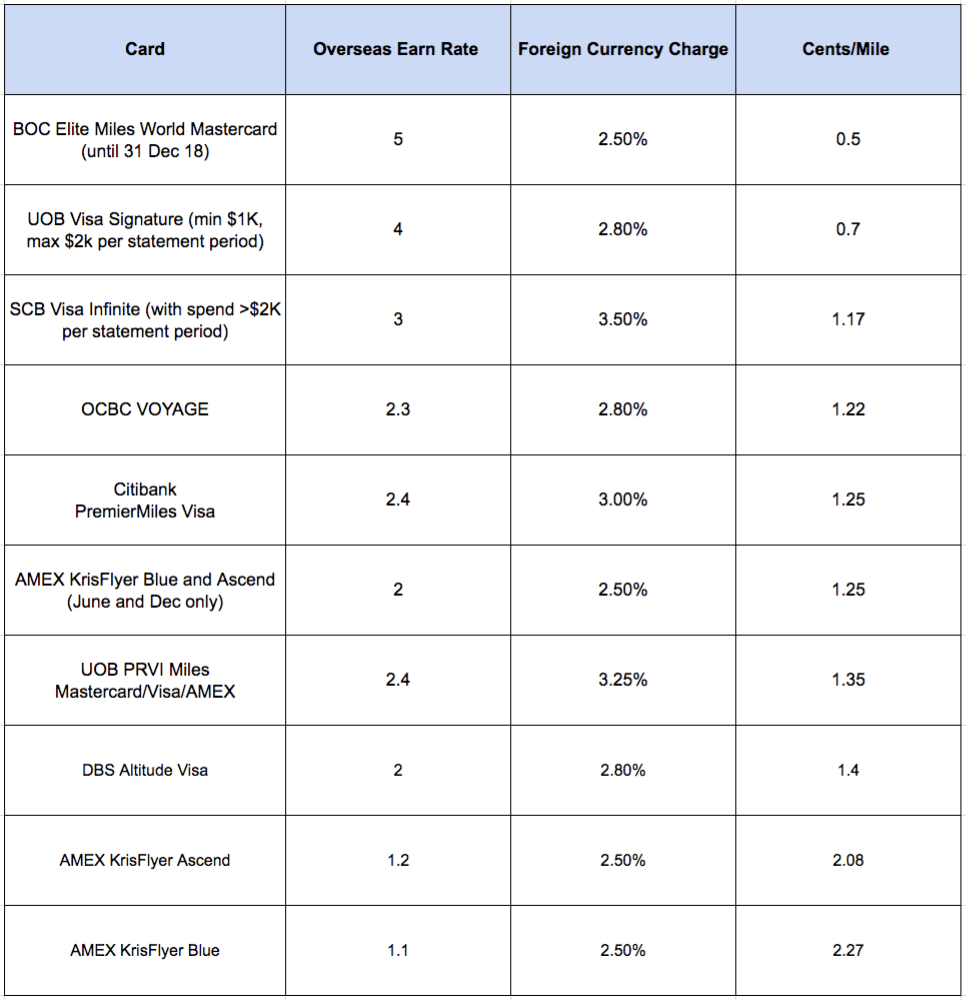

Of course, it's a bit pointless to look at the fees in isolation. You need to see how many miles you get when you incur those fees. In the table below I've looked at several popular miles cards, their overseas earn rates, charges and the cost you're paying for miles.

Perhaps you're wondering if it's worth paying that price for miles. The answer really depends on how much you value a mile. In general, buying miles at less than 2 cents is a decent price, although each person's individual valuation will differ depending on his or her circumstances.

To put it another way, it costs 176,000 miles to fly round trip from Singapore to San Francisco in Business Class. Assuming you acquired your miles at a cost of 0.5 cents per mile, you'd be paying the equivalent of S$880 (0.5 x 176,000), which is pretty impressive. That's purely hypothetical, though, as you'd need to spend S$35,200 overseas on the BOC Elite Miles World Mastercard alone for that to hold true.

In reality, most people's miles will be acquired from a range of sources: annual fees, overseas spending, as well as "zero cost" ways like paying for local purchases (zero cost in the sense that you don't pay any explicit cost to earn miles). You'd need to take all that into account when calculating your weighted average cost of mile acquisition.

I'm generally happy to use my miles earning cards overseas, because I believe the value I get out of the miles well exceeds the fees I pay. As you can see from the table above, not all cards are equal, so be sure to pick the right ones!

Other points to note about overseas card usage

As a security feature, most credit cards will have their overseas use feature disabled by default. You may need to contact your bank to get it activated before traveling.

Also, you may have been asked whether you want to "pay in Singapore Dollars" when traveling. Always say no.

Also, you may have been asked whether you want to "pay in Singapore Dollars" when travelling. Always say no. This option is known as Dynamic Currency Conversion (DCC), and you'll end up paying higher fees than if you used your bank's conversion rates. Here's an example from a trip I made to India:

The screenshot shows what UOB charged me (S$1,459.35), and the receipt above shows what I would have been charged if I opted for DCC (S$1,530.33). That should be enough to make most people shudder. To add insult to injury, you won't earn any overseas spending bonuses if you opt for DCC - you'll earn miles as if you used your card in Singapore.

Merchants earn a cut of the DCC fees, and some unscrupulous ones opt customers in for DCC without their consent. Don't assume you'll always be asked, and be sure to check what you're signing! Read what you can do to protect yourself against DCC here.

The safest way to avoid DCC is to use an American Express card, as AMEX cards do not support DCC.

Conclusion

Using your credit card overseas is not without cost, but the miles you earn may more than help make up for it. As long as you exercise basic common sense, like not letting your card out of your sight and not maxing out your credit limit on something you can't afford, there's no reason why you shouldn't pack along your plastic when you fly.

What to read next?

How (and How Not) To Get An Airline Upgrade

‘Why I Prefer Miles Over Cashback Cards, All Day, Every Day’

Travel Hacking Singapore Blog Teaches Anyone How to Fly on Business Class

Epic Trip Inspires Singapore Blogger to Share Travel Hacking Secrets

By Aaron Wong

Aaron started The Milelion to help people travel better for less and impress “chiobu”. He was 50% successful. This is his story.

Similar articles

Amex, Visa, or Mastercard: Which is Best for Travel?

Here’s Why You Should Never Use Air Miles Redemption for Economy Class

What’s A Hassle-free Way To Pay Overseas?

Best 6 Credit Cards For Overseas Spending

Should I Use A Credit Card Or Multi-Currency Card For Overseas Spending?

‘Why I Prefer Miles Over Cashback Cards Any Day, Every Day’

How Do You Value An Air Mile?

Credit Card Signup Bonuses: How to Maximise Miles with Big Ticket Spending

Back to Blog

Back to Blog