Opinions expressed reflect the view of the writer (this is his story).

It’s understandable why some people have reservations about using their credit cards for overseas spending. Horror stories about fraud, hefty bank fees and spending beyond one’s means abound, and most travellers resort to exchanging cash before they fly.

But if you’re in the miles and points game, you’ll know that using your credit card overseas can be a source of big rewards. That’s because banks want a share of your overseas wallet, and to do so, they dangle sizeable foreign currency spending bonuses on selected cards.

I’ve previously made the argument that it’s absolutely worth using your credit cards for overseas spending to earn miles, assuming you spend responsibly. The question then is, which cards should you be packing with you?

UOB Visa Signature

| Overseas Earn Rate | Foreign Transaction Fee | Cost Per Mile* | Notes |

| 4 mpd | 2.8% | 0.7 cents | 4 mpd applies for min S$1K max S$2K foreign currency spend per statement period |

*What’s a good price to pay per mile? Have a read of my post on valuing miles

The UOB Visa Signature (income req: $50K) may not be actively marketed by the bank anymore, but it’s still one of the best cards to bring overseas. That’s because it offers a hefty 4 miles per dollar (mpd) earn rate on foreign currency spending.

Some conditions apply- you need to spend at least S$1K in foreign currency in a statement period (be careful, because your statement period may not correspond to the calendar month!) to earn 4 mpd. Also, you don’t want to spend more than S$2K, because every incremental dollar above S$2K attracts only a measly 0.4 mpd.

Assuming you’re able to abide by these restrictions, then this card can earn you a tidy return on your vacation spending.

BOC Elite Miles World Mastercard

| Overseas Earn Rate | Foreign Transaction Fee | Cost Per Mile | Notes |

| 3 mpd | 3.0% | 1.0 cents | N/A |

The BOC Elite Miles World Mastercard (income req: $30K) has been making a splash in the Singapore miles and points game ever since its debut in July 2018.

Although the card no longer offers the whopping 5 mpd on foreign currency spending that it used to, the revised 3 mpd offering is still pretty attractive.

Cardholders earn 3 mpd on all foreign currency spending, without any cap or minimum spend required. As a bonus, you also enjoy four complimentary lounge passes, so you can relax en route to your vacation.

Standard Chartered Visa Infinite

| Overseas Earn Rate | Foreign Transaction Fee | Cost Per Mile | Notes |

| 3 mpd | 3.5% | 1.17 cents | 3 mpd applies if you spend at least S$2K in a month (overall) |

High-income earners may want to consider the SCB Visa Infinite (income req: $125K). This card gives 3 mpd on foreign currency spending without cap, so long as you spend at least S$2K in a month (the S$2K can include both local and overseas spending).

Cardholders also enjoy six complimentary Priority Pass visits a year, plus 35K bonus miles when they pay the first year’s $588.50 annual fee (non-waivable).

As an added bonus, SCB's instant approval and Digital credit card issuance also makes it a breeze for you to start racking up your points as soon as possible.

Standard Chartered Rewards+

| Overseas Earn Rate | Foreign Transaction Fee | Cost Per Mile | Notes |

| 2.9 mpd | 3.5% | 1.21 cents | 2.9 mpd capped at S$2,222 of foreign currency spending per card anniversary year |

The SCB Rewards+ card (income req: $30K) offers 1.45 mpd on dining and 2.9 mpd on overseas spending. No minimum spend is required, but the 2.9 mpd on overseas spending is capped at $2,222 per card anniversary year.

After that, you’ll earn a paltry 0.29 mpd. Therefore this card is best for those who don’t see themselves spending a lot overseas but who still want some miles to show for it.

OCBC VOYAGE

| Overseas Earn Rate | Foreign Transaction Fee | Cost Per Mile | Notes |

| 2.4 mpd | 3% | 1.25 cents | 2.4 mpd rate until 31 Dec 2019, thereafter 2.3 mpd |

From now till 31 December 2019, OCBC VOYAGE (income req: $120K) cardholders will earn 2.4 mpd on overseas spending, up from the usual 2.3 mpd. There is no minimum spending or cap.

The VOYAGE is an interesting product compared to the other cards here because you earn what’s called VOYAGE miles. These can be converted to KrisFlyer at a 1:1 ratio, but can also be used to offset the cost of revenue tickets on any airline, in any cabin class.

That’s beyond the scope of this post, but read this if you’re interested in learning more.

UOB PRVI Miles

| Overseas Earn Rate | Foreign Transaction Fee | Cost Per Mile | Notes |

| 2.4 mpd | 3.25% | 1.35 cents | 3 mpd applies if you spend at least S$2K in a month (overall) |

The UOB PRVI Miles cards (income req: $30K) continue to be a good option for overseas spending with a 2.4 mpd earn rate. There is no minimum spend or cap applicable, and to sweeten the deal, the UOB PRVI Miles AMEX allows you to unlock two complimentary airport transfers when you spend at least S$1K in foreign currency in a quarter.

What about other cards?

The cards listed above are good for general spending overseas. However, if you have specific types of spending in mind, you can also make use of some of the following:

- Citi Rewards Visa: 4 mpd on overseas shopping

- OCBC Titanium Rewards: 4 mpd on overseas shopping

- UOB Lady’s Card: 4 mpd on your choice of overseas dining, entertainment, fashion, transport, beauty & wellness, or travel

For more information, check out this post on best shopping cards for earning miles.

A final word about DCC

It would be remiss to talk about using your credit card overseas without a warning about DCC (dynamic currency conversion). Simply put, always say no when asked if you want to process your transaction in SGD.

Why? Because the merchant and payment processor build in a margin into this conversion that always leaves you worse off. You’d be much better off using your bank’s rate instead.

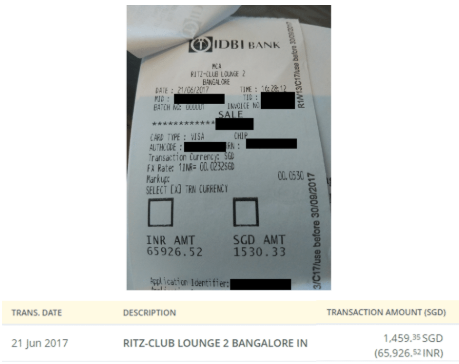

The receipt above shows an incident I experienced at a hotel in India – at the time of checkout, I had the option to pay in the local currency of INR 65,926 or take the hotels’ DCC rate of S$1,530. I opted for the local currency, and sure enough, UOB’s converted figure was only S$1,459, way below what the DCC rate would have been!

Furthermore, had I chosen to do DCC, I would not have earned the 4 mpd on my UOB Visa Signature card because the transaction would be processed in SGD.

I hope this illustrates why DCC is a universally bad option to take – don’t fall for it!

Conclusion

Using your card overseas need not be a source of stress. In fact, used properly, it’s one of the fastest ways to chalk up miles. Guard your card carefully, don’t spend more than you’ve budgeted and before you know it, you’ll be earning your way to your next vacation.

Compare and apply for the best credit cards through SingSaver

Keen on applying for any of the above credit cards? Do it through SingSaver and receive additional sign-up bonuses on top of the bank's own welcome gifts! Alternatively, compare the best air miles cards with our handy SingSaver comparison tool to find whichever suits your needs the best.

Read these next:

Which Are The Best Cards to Earn Miles While Shopping?

What Are The Best Ways To Pay For Big-Ticket Items in Singapore?

Air Miles Cards: 8 Questions to Help You Choose the Right Card

The Best Miles Cards… May Be Rewards Cards

6 Credit Cards That Give You Free Access to Airport Lounges

By Aaron Wong

Aaron started The MileLion to help people travel better for less and impress “chiobu”. He was 50% successful. This is his story.

Similar articles

6 Ways to Turbocharge Your Travel Hacking Game

Which Are The Best Cards To Earn Miles While Shopping?

Best Credit Cards For Overseas Spending in Singapore

SC EasyBill Vs Citi PayAll: Which Is Better?

‘I Have 19 Credit Cards But There’s Just 3 I Would Recommend Anyone to Have’

Which Credit Card Is The Best Companion For VTL Travel?

Should I Use A Credit Card Or Multi-Currency Card For Overseas Spending?

Should I Use Credit Cards Overseas to Earn Miles?

Back to Blog

Back to Blog